How War and Economic Uncertainty Affect Your Health Insurance in 2026

ACA premiums are already up 18-20% in 2026 — the largest increase since 2018. The Iran conflict is accelerating inflation across housing, gas, and groceries. Here's what that means for your health coverage and the one option that's insulated from all of it.

Private PPO • ACA • Self-Employed • 2026

How the Iran Conflict Is Affecting Health Insurance Costs in 2026 — And What to Do About It

The numbers before we even get to the war

Before the Iran conflict became a factor, the 2026 health insurance picture was already the worst in nearly a decade. Enhanced ACA subsidies that had been in place since 2021 expired at the end of 2025. The impact was immediate and severe.

(Peterson-KFF Health System Tracker)

(KFF Survey, March 2026)

(KFF Survey, March 2026)

That's the baseline. Now add the Iran conflict.

How the Iran conflict accelerates the problem

War doesn't directly change your health insurance premium. But it does drive inflation — and inflation drives health insurance costs through several channels that are already under pressure in 2026.

How conflict drives health costs up

- Oil price spikes → higher logistics and supply chain costs for medical supplies and pharmaceuticals

- Broader inflation → hospitals and providers raise prices to cover operating costs

- Drug manufacturing disruption → specialty medication costs increase

- Labor cost inflation → medical staffing gets more expensive

- Economic anxiety → delayed care followed by higher-acuity claims

What's already happened

- Gas prices up following Feb. 28 Iran conflict onset

- Grocery inflation accelerating in Q1 2026

- Insurers projecting 7–8% medical cost trend for 2026

- Specialty drug costs rising double digits

- ACA risk pool shrinking as healthy enrollees exit — driving remaining costs higher

ACA vs Private PPO — How each responds to economic uncertainty

- Premium set by government policy and insurer filings — already up 18–20%

- Subsidy dependency — if Congress changes policy, your cost changes

- Risk pool shrinking — fewer healthy enrollees means higher costs for those remaining

- Inflation passes through to premiums at renewal

- No control over what happens to your rate next year

- Enrollment windows — can't act outside of SEP or open enrollment

- Premium based on your health — not income, not politics

- No subsidy dependency — zero exposure to Congressional action

- Not part of the ACA risk pool — unaffected by pool deterioration

- Rate locked at underwriting — no surprise renewals mid-year

- Available any month — no enrollment window dependency

- Nationwide PPO network — works in any state, any economic environment

Who benefits most from switching right now

Self-employed & 1099

- Freelancers, consultants, contractors

- Above subsidy threshold — paying full ACA rate

- Health-based pricing often significantly lower

- Available any month — no waiting for enrollment

Small business owners

- No group plan — buying individually

- Current ACA rate jumped 18–20% at renewal

- Private PPO not tied to ACA rate filings

- Rate set at underwriting — predictable going forward

Real estate, gig & commission earners

- Variable income — ACA subsidy reconciliation creates tax risk

- Private PPO has zero income reporting requirement

- No subsidy clawback at tax time

- Premium stays consistent regardless of income year

We compare your current ACA cost against private PPO options for your health profile. Most healthy self-employed applicants are surprised how much the difference is. Free quotes, no obligation, no pressure.

What private PPO actually costs right now

For healthy applicants, private medically underwritten plans price based on age and health — not on whatever the ACA risk pool is doing or what Congress decided about subsidies. Current approximate ranges for healthy non-smokers in 2026:

Age 25–35

- $120–$240/month typical range

- $0 deductible plans available

- Nationwide PPO access

- Lowest rates in your lifetime

Age 35–50

- $220–$430/month typical range

- Multiple deductible options

- Often 30–50% less than current ACA full rate

- Rate locked at approval

vs ACA unsubsidized 2026

- Silver plan: $350–$550/month

- Gold plan: $450–$650/month

- Up 18–20% from 2025

- Further increases likely in 2027

*Private PPO ranges are illustrative estimates for healthy non-smokers. Actual premiums vary by age, state, health history, plan, and underwriting outcome. ACA estimates based on 2026 market data for unsubsidized enrollees.

Frequently Asked Questions

Does war directly affect my health insurance premium?

Not directly — wars don't trigger immediate premium changes. But armed conflict drives inflation through energy prices, supply chains, and labor costs. Those inflationary pressures flow into healthcare costs over time, which insurers factor into the following year's premium filings. ACA premiums were already elevated in 2026 before the Iran conflict. The conflict adds additional inflationary pressure on an already stressed system.

Will ACA premiums go up again in 2027?

Based on current trends — continuing inflation, a shrinking and sicker ACA risk pool, rising drug costs, and geopolitical uncertainty — further increases in 2027 are likely. Insurers are already seeing the spiral effect: as healthy people exit the ACA market, remaining costs rise for those who stay, which drives more healthy people out. Private PPO exits this cycle entirely because it's individually underwritten, not pool-based.

What if the subsidies come back?

Subsidy reinstatement would reduce ACA costs for those who qualify by income. But it wouldn't help anyone above the subsidy threshold — and it comes with a perpetual political risk that subsidies can be changed or removed again. Private PPO has no subsidy dependency in either direction. Your rate is based on your health at the time of underwriting, period.

Can I switch from ACA to private PPO mid-year?

Yes. Private medically underwritten plans are available any month of the year with no enrollment window. If you're approved, your coverage can start as soon as the following month. You'd cancel your ACA plan once the private plan is active — typically timing it for a clean month-to-month transition with no gap.

What if the conflict escalates — could that affect private PPO plans?

Private PPO plans are not war risk insurance — they cover domestic healthcare costs the same way in any geopolitical environment. Broader inflation could eventually affect private plan renewal rates, but private plans adjust individually at renewal rather than through the systemic ACA pool mechanism. And importantly, you lock in your rate at underwriting — it doesn't change mid-year regardless of what happens.

Who doesn't qualify for private PPO?

Private medically underwritten plans require a health questionnaire. Applicants with significant health history — active chronic conditions, recent hospitalizations, multiple ongoing medications — may not qualify. For those individuals, ACA marketplace coverage remains the right path. We'll tell you honestly which option makes sense for your situation before you apply for anything.

We're an independent broker licensed in 32 states. We compare your ACA cost against private PPO options based on your exact health profile and tell you honestly what makes sense. No pressure, no obligation.

Robert Adams * President & Licensed Agent * NPN 19540130 * Licensed in 32 states. Statistical data sourced from KFF Survey (March 2026), Peterson-KFF Health System Tracker (January 2026), Commonwealth Fund (September 2025), and CNBC (March 2026). Premium estimates are illustrative ranges and are not guaranteed. Actual premiums vary by age, state, tobacco status, plan selection, carrier, and underwriting outcome. Private medically underwritten plans are not ACA-compliant and are subject to medical underwriting — not all applicants qualify. This content is for informational purposes only and does not constitute insurance, financial, or legal advice.

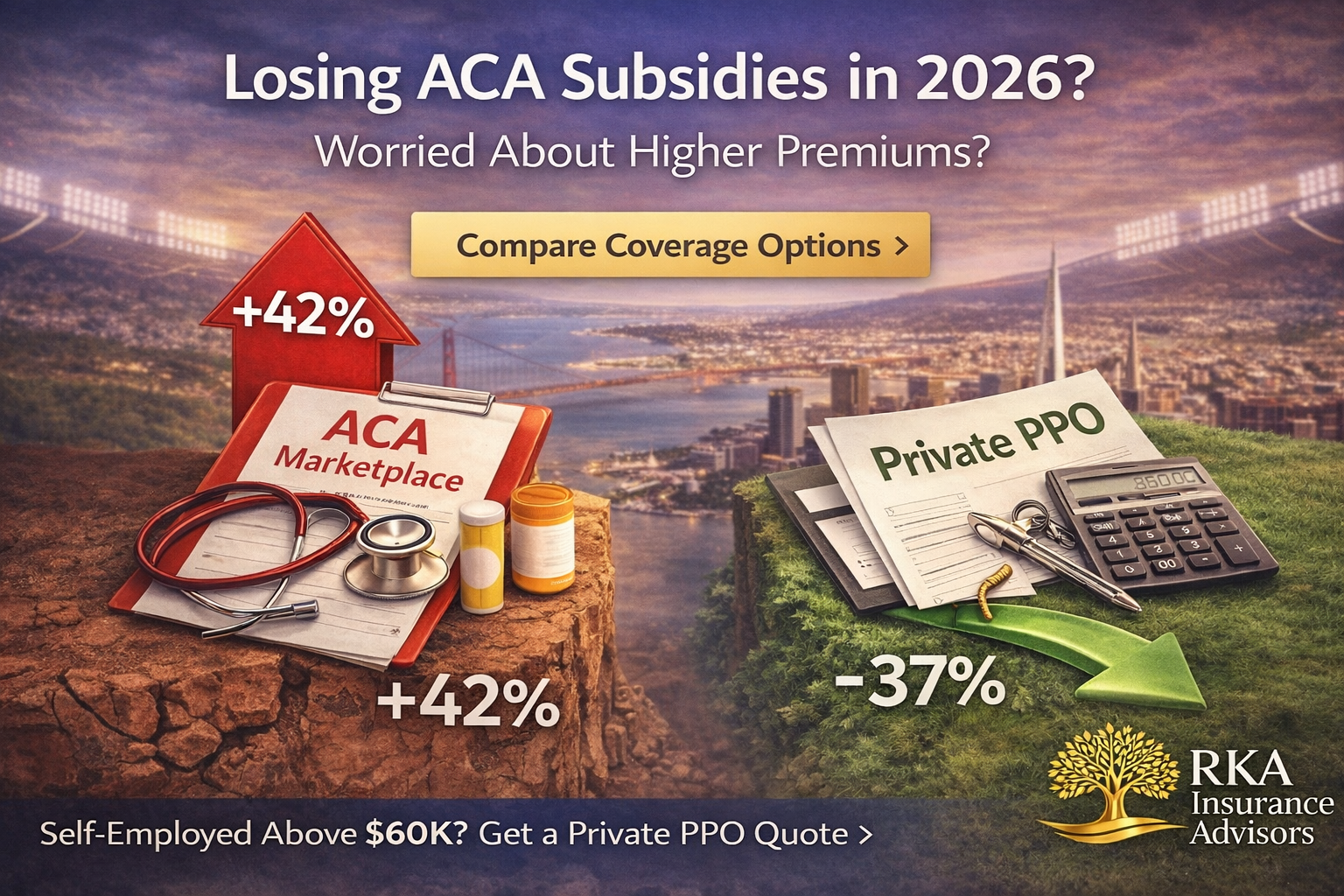

ACA Subsidy Cliff 2026: What Self-Employed Earners Above $60K Need to Know

Enhanced ACA subsidies expired December 31, 2025. If you earn above $60,240, you now pay the full unsubsidized Marketplace premium. Here's what changed — and what self-employed professionals in good health can do about it.

Private PPO * ACA 2026 * Self-Employed

ACA Subsidy Cliff 2026: What Self-Employed Earners Above $60K Need to Know

What changed in 2026

Before (2021-2025)

- Enhanced credits capped premiums at 8.5% of income

- Subsidies available at any income level

- Higher earners still got meaningful help

Now (2026)

- Subsidies cut off at $60,240 (individual)

- Above that - 100% full unsubsidized rate

- Full-price Silver plans average $600-$900/mo*

- Deductibles typically $4,000-$8,000

Marketplace vs Private PPO

- Guaranteed issue - no health screening

- Subsidies if income under $60,240

- Often HMO/EPO - referrals common

- Open enrollment window only

- Income reconciliation at tax time

- Full price if above subsidy threshold

- Health underwriting required

- Premiums based on health - not income

- Nationwide PPO access - no referrals

- Available any month - no enrollment window

- No subsidy reconciliation at tax time

- Can cost significantly less for healthy applicants*

Who Private PPO works best for

Income above $60K

- No subsidies available anyway

- Private PPO often cheaper

Variable income

- No mid-year reconciliation risk

- Fixed premium regardless of earnings

Missed open enrollment

- No qualifying event needed

- Coverage can start within days

How RKA helps

What we do

- Confirm your exact subsidy eligibility

- Verify your doctors in both ACA and PPO networks

- Project total annual cost - premium + deductible

- Pre-screen PPO eligibility before you apply

What you get

- Side-by-side ACA vs PPO comparison

- No surprises at application or tax time

- Coverage that fits your income and health

- A licensed advisor - not a call center

We verify your doctors, check your prescriptions, and compare ACA vs private PPO with real numbers. No pressure, no obligation.

Frequently Asked Questions

What is the ACA subsidy cliff in 2026?

The income point where premium tax credits phase out entirely - $60,240 for individuals in 2026. Earn $1 above that and you pay the full unsubsidized rate.

Are private PPO plans available if I missed open enrollment?

Yes. Private medically underwritten PPO plans are available year-round. No qualifying life event required.

How much could I save with a private PPO?

It depends on your age, state, and health history. For healthy applicants above the subsidy threshold, savings can be significant. We run the exact comparison for your situation at no cost.

What does medically underwritten mean?

The insurer reviews your health history before approving coverage. We pre-screen your eligibility so you know where you stand before submitting a full application.

Robert Adams * President & Licensed Agent * NPN 19540130 * Licensed in 30 states. For educational purposes only. *Premium estimates based on publicly available 2026 rate data and vary significantly by age, state, and plan. Speak to a licensed advisor for exact figures.

Super Bowl Health Insurance Playbook: Coverage Tips for Game Day and Beyond

Super Bowl LX is here—Patriots vs Seahawks at Levi's Stadium. From party injuries to travel emergencies, here's your health insurance playbook for game day and beyond. Private PPO plans available year-round.

Super Bowl Health Insurance Playbook: Coverage Tips for Game Day and Beyond

Fast take: Super Bowl LX is here—Patriots vs Seahawks—and whether you're hosting a party, traveling to San Francisco, or watching from home, it's a good time to think about your health coverage. From party injuries to travel emergencies, here's what you need to know.

Need coverage before the big game?

Private PPO plans are available year-round—no Open Enrollment required.

Get Free Quotes Book a CallSuper Bowl by the numbers

Game Day Stats

✓ 115+ million viewers expected

✓ 1.4 billion chicken wings consumed

✓ 325 million gallons of beer

✓ Second-largest food consumption day in the U.S.

Health Risks Spike

✓ Heart attacks increase 25% during high-stakes games

✓ ER visits spike for burns, cuts, falls

✓ Food poisoning from buffet food left out

✓ Alcohol-related incidents at 10-year high

Common Super Bowl injuries (and what they cost without insurance)

Kitchen & Grill Injuries

Deep fryer burns: $3,000–$15,000+ (ER + treatment)

Knife cuts requiring stitches: $500–$2,500

Grease fire burns: $5,000–$50,000+

Food poisoning (severe): $1,500–$8,000

Party & Celebration Injuries

Slip and fall (broken wrist): $7,500–$20,000

Alcohol poisoning (ER): $2,000–$10,000

Heart attack (game stress): $50,000–$200,000+

Fireworks injury: $5,000–$100,000+

⚠️ Uninsured? These costs come straight out of your pocket.

The average ER visit costs $2,200 without insurance. A single Super Bowl party mishap can wipe out your savings—or worse, lead to medical debt that follows you for years.

Traveling to the Bay Area for the game?

What to check before you go

✓ Does your plan cover out-of-state emergencies?

✓ Are there in-network hospitals in the Bay Area?

✓ What's your out-of-network ER coverage?

✓ Do you have telehealth for minor issues?

HMO vs PPO for travel

HMO: May only cover emergencies out-of-state

HMO : Referrals Required

Nationwide PPO: Broad coverage across states

Nationwide PPO: No Referrals required

Game day health tips

Food safety

✓ Don't leave food out more than 2 hours

✓ Keep hot foods above 140°F

✓ Keep cold foods below 40°F

✓ Never refreeze thawed wings

Heart health

✓ Know your limits—stress raises blood pressure

✓ Take breaks during intense moments

✓ Don't mix excessive alcohol + salty snacks

✓ Know heart attack warning signs

Who needs coverage before kickoff?

You should get covered if...

✓ You missed Open Enrollment (Jan 15 deadline passed)

✓ You're currently uninsured

✓ You're between jobs

✓ COBRA is too expensive

✓ You travel frequently and need nationwide coverage

Private PPO advantages

✓ Enroll any time—no waiting for Open Enrollment

✓ Nationwide PPO networks

✓ No referrals needed for specialists

✓ Out-of-network coverage available

✓ Coverage can start within days

Don't let a Super Bowl mishap become a financial disaster

Get covered before the game. We'll compare options and find the right plan for you.

Get Free Quotes Book a CallQuick FAQs

Can I get health insurance today before the game?

Private PPO plans can be applied for any day, but coverage typically starts the 1st or 15th of the following month. For immediate coverage, some plans offer faster start dates—contact us to discuss your options.

I missed Open Enrollment. Am I stuck without coverage?

No. Private PPO plans are available year-round and don't require a Qualifying Life Event. If you don't qualify for a Special Enrollment Period, private plans may be your best option.

Will my insurance cover an ER visit in another state?

Most plans cover emergency care anywhere, but costs vary significantly. HMOs may only cover true emergencies at out-of-network rates. PPOs typically offer broader out-of-state coverage. Check your plan details before traveling.

What counts as a "medical emergency" at a Super Bowl party?

True emergencies include heart attacks, severe burns, broken bones, choking, allergic reactions, and alcohol poisoning. Minor cuts, mild food poisoning, or hangovers typically don't qualify for emergency coverage at in-network rates.

Go Patriots! (Or Seahawks—we cover fans of both teams.) For education only. Eligibility and benefits vary by carrier and state. Always review official plan documents.

Starting a New Business? Here's Your Health Insurance Game Plan

Starting a new business with unpredictable income? Private underwritten PPOs eliminate subsidy reconciliation hassles and may offer plans with deductibles as low as $0—often beating ACA high-deductible plans with healthier risk pools and supplemental coverage.

Starting a New Business? Here's Your Health Insurance Game Plan

Fast take: Left your job to start a business? Your health insurance strategy matters as much as your business plan. With unpredictable first-year income, private underwritten PPOs eliminate subsidy reconciliation hassles and may offer plans with deductibles as low as $0—often beating high-deductible ACA plans with better networks and lower total costs.

Just went full-time on your business?

We'll compare COBRA, ACA, and private PPO options—and verify your doctors stay covered while you build.

Get Free Quotes Book a CallYour coverage options when starting a business

COBRA (Bridge Option)

✓ Keep your old employer plan

✓ Same doctors and networks

✗ Usually most expensive

✗ Time-limited (18 months max)

ACA Marketplace

✓ May be cheapest with subsidies

✓ Loss of job = Special Enrollment

✗ Often HMO/EPO networks

✗ Income reconciliation at tax time

✗ High deductibles ($7,000-$9,000+)

Private Underwritten PPO

✓ May qualify for deductibles as low as $0

✓ Nationwide PPO access

✓ Year-round enrollment

✓ No income reporting

✓ Healthier risk pools

Why unpredictable income is a nightmare with ACA subsidies

The income estimation trap

When you enroll in ACA, you estimate your 2026 income in advance. First-year business? You're guessing.

✗ Estimate too low → subsidy payback at tax time

✗ Estimate too high → overpay premiums all year

✗ Business takes off mid-year? You owe thousands back

Private PPO eliminates the guessing game

Your premium is based on age, ZIP, and plan—not income.

✓ Make $50k or $500k? Premium stays the same

✓ No Form 8962 reconciliation at tax time

✓ Budget with confidence from day one

Why private underwritten PPOs beat high-deductible ACA plans

Many entrepreneurs think high-deductible Marketplace plans are their only affordable option. That's rarely true for healthy business owners.

ACA high-deductible plans

✗ $7,000-$9,000+ deductibles common

✗ You pay 100% until deductible is met

✗ Risk pool includes all applicants (healthy + unhealthy)

✗ Often HMO/EPO with referral requirements

✗ Premium jumps if income rises

Private underwritten PPOs

✓ May qualify for deductibles as low as $0

✓ Copays often start immediately (office visits, Rx)

✓ Risk pool = healthy small business owners/employees

✓ Nationwide PPO networks, no referrals

✓ Premium never changes with income

The risk pool advantage: Why private plans cost less for healthy entrepreneurs

ACA Marketplace risk pools

Guaranteed issue = everyone accepted regardless of health

Risk pool includes:

• Healthy applicants

• Chronic conditions

• High-cost ongoing treatments

Result: Higher premiums spread across everyone, including you

Private underwritten risk pools

Medical underwriting = healthier risk pool through association memberships

Risk pool includes:

• Healthy business owners

• Small business employees

• Self-employed professionals

Result: Lower premiums for healthy applicants, better benefits, lower deductibles

Supplemental coverage: Offsetting out-of-pocket costs

Even with low-deductible private PPOs, you can further reduce financial risk with supplemental coverage:

Hospital indemnity insurance

Pays cash benefit per day of hospitalization

✓ Use cash for deductibles, copays, or lost income

✓ Low monthly cost ($30-$80/month typical)

Accident insurance

Covers ER visits, urgent care, broken bones, imaging

✓ Pays lump sum or per-service benefits

✓ Complements your major medical plan

Critical illness insurance

Lump-sum payment if diagnosed with covered condition (heart attack, stroke, cancer)

✓ Use for medical bills, travel, mortgage—anything

✓ Peace of mind for catastrophic events

Strategy: Layer your protection

Private PPO with low deductible + hospital indemnity ($500/day) = near-zero financial risk

Total monthly cost often less than ACA high-deductible plan alone

Why entrepreneurs choose private PPO plans

No income reconciliation headaches

Your premium doesn't change when your business revenue fluctuates. No Form 8962, no tax-time surprises, no subsidy payback.

Travel-friendly nationwide networks

Client meetings in Austin? Conference in Denver? PPO access means you're covered wherever business takes you—no network restrictions.

Direct specialist access

No primary care referrals. No waiting weeks for authorization. See specialists when you need them without bureaucratic delays.

Lower total annual costs

Low-deductible PPO often costs less annually than $8,000 deductible ACA plan when you factor in total out-of-pocket exposure.

Common mistakes new business owners make

❌ Staying on COBRA too long

COBRA is expensive and time-limited. It's a bridge, not a long-term solution. Compare alternatives within 60 days.

❌ Underestimating income for subsidies

Business takes off? You'll owe subsidy money back at tax time. Estimate conservatively or skip subsidies entirely with private PPO.

❌ Accepting high deductibles as inevitable

ACA high-deductible plans aren't your only option. Private underwritten PPOs may offer plans with deductibles as low as $0 for healthy applicants.

❌ Not considering supplemental coverage

Hospital indemnity and accident insurance can eliminate remaining out-of-pocket exposure for less than $100/month.

Decision guide: Which option fits your business?

Choose ACA Marketplace if...

✓ Your first-year income will be very low (under $35k individual)

✓ You qualify for strong subsidies and cost-sharing reductions

✓ Your income is stable and predictable

✓ You're comfortable with high deductibles and HMO networks

✓ You don't mind annual tax reconciliation

Choose Private Underwritten PPO if...

✓ Your income is variable or growing (startup revenue unpredictable)

✓ You're healthy and pass medical underwriting

✓ You want lower deductibles and immediate copays

✓ You travel frequently for business

✓ You prefer nationwide PPO access with no referrals

✓ You want to avoid subsidy reconciliation at tax time

Your launch timeline: Health insurance edition

Before you leave your job

✓ Document your last day of employer coverage

✓ Get COBRA election notice

✓ List your current doctors and prescriptions

✓ Estimate your Year 1 business income range (low and high scenarios)

First 60 days after leaving

✓ Compare COBRA vs ACA vs private PPO costs and deductibles

✓ Verify provider networks for all options

✓ Get quotes for supplemental coverage (hospital indemnity, accident)

✓ Enroll in your long-term solution before Special Enrollment window closes

First year in business

✓ Track actual income monthly (if on ACA, update estimates)

✓ Keep records for self-employed health insurance tax deduction

✓ Set aside emergency fund for deductibles and out-of-pocket costs

✓ Review supplemental coverage needs as business stabilizes

Annual review

✓ Reassess coverage during Open Enrollment (or anytime with private PPO)

✓ Compare costs as your income stabilizes

✓ Verify doctors are still in-network

✓ Adjust deductible level based on actual business cash flow

How RKA helps entrepreneurs

Fast transition planning

We map your options before your last day of work—COBRA bridge strategies, Special Enrollment timing, and private PPO alternatives with accurate underwriting pre-screening.

Network verification

We confirm your doctors and hospitals are in-network across all options—ACA, private PPO, and supplemental plans—before you commit.

Total cost analysis

We model multiple income scenarios and compare: premiums + deductibles + expected usage + supplemental coverage = your true annual cost.

Supplemental layering strategy

We show you how hospital indemnity, accident, and critical illness coverage can eliminate remaining out-of-pocket exposure affordably.

Launching your business? Lock your health insurance first.

We'll compare COBRA, ACA, and private underwritten PPO options—verify your doctors—and layer supplemental coverage to eliminate financial risk.

Get Free Quotes Book a CallQuick FAQs

Why is private underwritten PPO cheaper than ACA high-deductible if I'm healthy?

Risk pool matters. ACA pools include everyone regardless of health, spreading costs across healthy and unhealthy. Private underwritten plans pool healthy small business owners, employees, and self-employed professionals through association memberships, resulting in lower premiums and better benefits.

What if my business income is unpredictable?

Private PPO eliminates the guessing game. Your premium is based on age and ZIP—not income. Make $50k or $500k, your premium stays the same. No subsidy reconciliation, no Form 8962, no tax-time surprises.

How does supplemental coverage work with my major medical plan?

Supplemental policies (hospital indemnity, accident, critical illness) pay cash benefits directly to you—use the money for deductibles, copays, lost income, or anything else. They stack on top of your major medical plan to eliminate financial risk.

For education only; consult a tax professional for deduction advice. Eligibility for private underwritten plans subject to medical underwriting. Benefits vary by carrier and state. Always review official plan documents.

Avoid Tax Penalties: Navigating Health-Insurance Income Reporting (2025–2026) | RKA

Taking ACA premium credits? Keep your income estimate current and reconcile correctly to avoid surprise tax bills. Here’s how MAGI works, when to update, and how RKA helps.

Guides • Taxes & Reporting

Avoid Tax Penalties: Navigating Health-Insurance Income Reporting

Fast take: If you get ACA premium tax credits, your final subsidy is based on your actual year-end income (MAGI). To avoid surprise tax bills, keep estimates current, report life changes quickly, and reconcile correctly at tax time.

MAGI 101: What actually counts

- Start with AGI (from your 1040), then adjust for items like tax-exempt interest and nontaxable Social Security.

- Household MAGI includes the income of everyone on the return who must file taxes, not just the policyholder.

- Self-employed? Use net profit (after allowable business expenses), and revisit as the year unfolds.

Update income at the right times

- After big changes: new contract, raise/bonus, switching jobs, adding/removing a dependent, or moving.

- Quarterly check-ins: especially for variable/1099 income—prevents large year-end paybacks.

- Document it: keep notes on when/why you updated; it helps at tax time.

A simple, low-stress workflow

- Estimate annual MAGI (with a conservative range).

- Choose a plan; take only the advance credit you’re comfortable with.

- Track YTD income and adjust through your Marketplace account when needed.

- At tax time, reconcile with Form 1095-A and Form 8962.

Self-employed tips

- Buffer fund: set aside part of any premium savings for potential reconciliation.

- HSA strategy: if you’re in an HSA-eligible plan, contributions may lower MAGI.

- Quarterly rhythm: align income updates with your estimated tax payments.

Quick FAQs

What if I overestimated income?

Do I need to report small fluctuations?

Can you update my application for me?

This article is educational and not tax advice. Eligibility and benefits vary by carrier and state. Consult your tax professional about your specific situation.

OPEN ENROLLMENT IS HERE

Open Enrollment is open. 2026 premiums, networks, and deductibles are changing again. Here’s what to check now to avoid paying more or losing your doctors.

ENROLLMENT HELP • OPEN ENROLLMENT 2026

Written by Robert Adams

Open Enrollment Is Here: How to Avoid a Bad 2026 Plan

Open Enrollment is the short window each year when you can reset your coverage for the next calendar year. For 2026, premiums, deductibles, and networks are all shifting again. If you simply let your plan auto-renew, you could end up paying more, losing doctors, or getting stuck with the wrong deductible. Here’s what to do while Open Enrollment is open.

Key Dates While Open Enrollment Is Active

Open Enrollment Window

- Normally runs November 1st through mid-January

- Best time to compare plans before 2026 rates fully kick in

Priority Deadline

- Mid-December cutoff for a January 1st start

- Miss this and your new plan may not start until February

Final Change Deadline

- Last day of Open Enrollment is usually mid-January

- After this, changes typically require a qualifying life event (SEP)

Why You Shouldn’t Just Auto-Renew

- Your 2025 plan can come back in 2026 with new premiums and out-of-pocket costs.

- Doctor and hospital networks can quietly change—your provider may no longer be in-network.

- Prescriptions may move to a different tier or require new prior authorizations.

- If you don’t actively review options, you could pay more for less coverage all year long.

Marketplace vs Private PPO: What to Check Right Now

If You’re on the ACA Marketplace

- Re-run your income and household size—tax credits can change year to year.

- Confirm your doctors and main hospitals are still in-network.

- Review deductibles, copays, and out-of-pocket maximums for 2026.

- Watch for HMO/EPO restrictions and referral rules.

If You Qualify for Private PPO Options

- Check nationwide PPO access if you travel or live in more than one state.

- Confirm no referral requirements for specialists when eligible.

- Compare total cost: premium + expected usage, not just the monthly price.

- Good fit for self-employed, 1099, and families who want provider flexibility.

Want the right 2026 plan for your ZIP?

During Open Enrollment, we’ll verify your doctors and prescriptions, compare Marketplace and Private PPO options, and lay out the numbers in plain English before you decide.

FAQ

Do I have to re-apply every Open Enrollment?

What if I miss the mid-December deadline?

Can you help me compare Marketplace vs Private PPO?

Open Enrollment 2026 • health insurance deadlines • ACA Marketplace plans • Private PPO plans • health insurance quotes • RKA Insurance Advisors • self-employed health coverage

Robert Adams

https://www.RKAInsuranceAdvisors.com