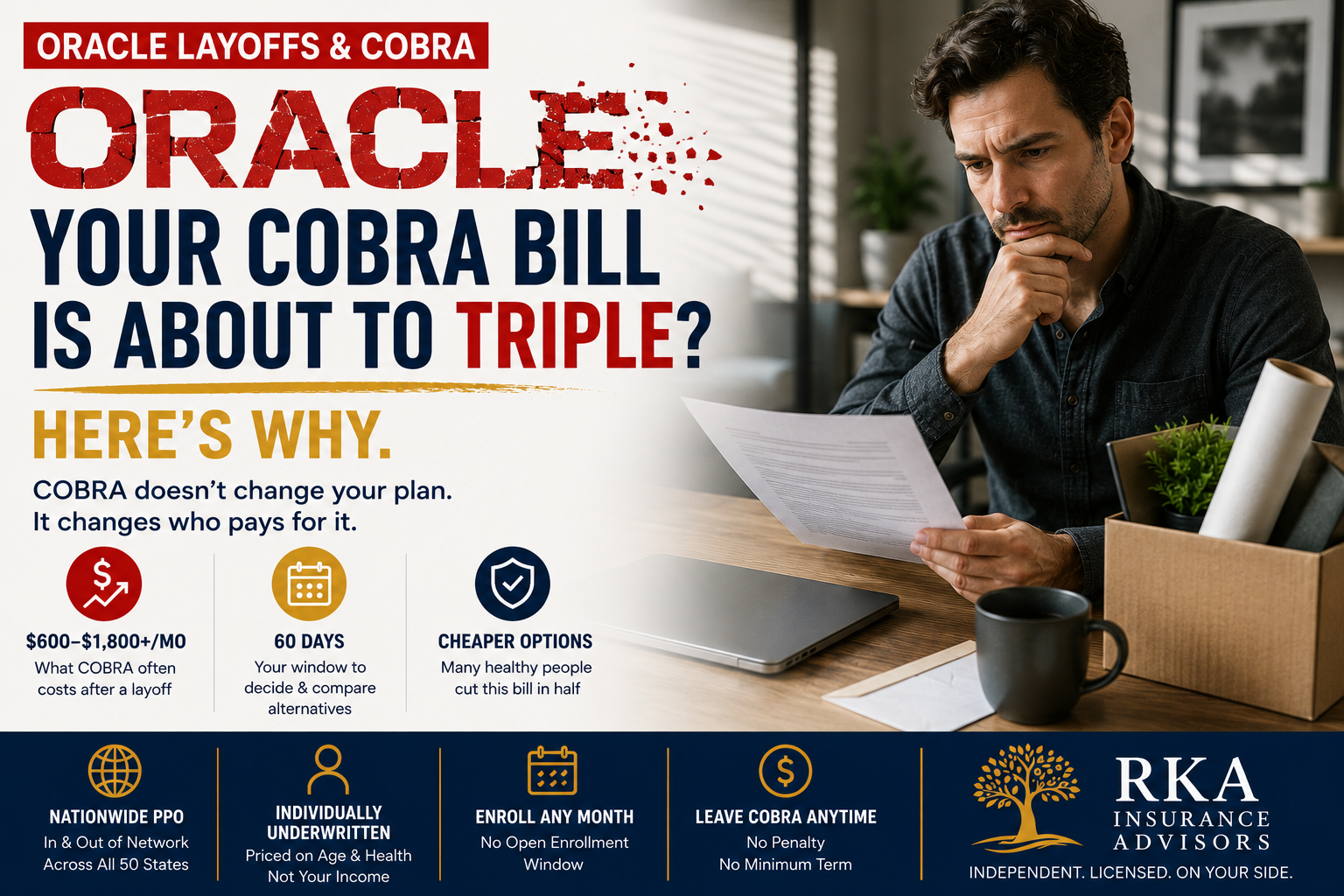

Oracle Layoffs & COBRA: What Your Coverage Will Cost and Cheaper Alternatives

Oracle cut roughly 21,000 roles over the past year. If you were one of them, the COBRA letter in your inbox is about to show you what your health plan actually costs. Here's how COBRA, ACA, and a nationwide private PPO compare —and how healthy people frequently cut the bill in half.

Layoffs & Coverage • COBRA • Private PPO

Oracle Layoffs & COBRA: What Your Coverage Will Cost and Cheaper Alternatives

Why the Oracle COBRA number is such a shock

While you were employed, Oracle carried most of your premium. You saw a modest payroll deduction and never saw the rest. Many Oracle employees have described the company covering only about half of the dependent cost even while employed — which means if you had a family on the plan, you were already paying more than most people do.

COBRA doesn't change your plan. It changes who pays for it. The coverage is identical — same doctors, same pharmacy, same network — but now 100% of the group premium is yours, plus the administrative fee. That's the entire reason the number looks nothing like what you're used to.

Your three real options after an Oracle layoff

COBRA

- Identical plan — zero disruption

- Same doctors and pharmacy

- No health questions

- Retroactive if elected within 60 days

- You pay the full premium — yours and Oracle's

- Plus up to 2% in admin fees

- Ends at 18 months

ACA Marketplace

- Guaranteed issue — no health screening

- Job loss opens a Special Enrollment Period

- Subsidies possible if this year's income drops

- Networks are often regional HMO/EPO

- Severance counts toward income — it can push you past the subsidy line

- Full price if your income stays high

Private PPO (underwritten)

- Priced on your health and age, not your income

- Nationwide PPO access — specialists without referrals

- Available any month — no enrollment window

- No subsidy reconciliation at tax time

- Frequently 30–50% below COBRA for healthy applicants

- Medical underwriting — not everyone qualifies

The severance trap nobody mentions

Your severance is income. If you're counting on an ACA subsidy to make a marketplace plan affordable, run the math on your full-year projected income — severance included. A large lump sum can push you over the subsidy threshold for the year, and the marketplace reconciles that at tax time on Form 8962. People get a subsidy all year, then owe it back. A private PPO doesn't have this problem at all: the premium is set by age and health, so it doesn't care what your severance was or when you land your next role.

How to use your 60-day window correctly

Do this first

- Apply for a private plan now — underwriting takes 2–4 weeks

- Don't elect COBRA on day one; you don't have to

- If approved, coverage starts the first of next month

- If underwriting runs long, elect COBRA retroactively as a backstop

If you already elected COBRA

- You can leave COBRA any month — no penalty, no minimum

- Private plans have no enrollment window

- Cancel COBRA once the new plan activates

- Time it to the first of the month and there's no gap

Plenty of people ride COBRA for the full 18 months without realizing they could have left at any point. If you're three or six months in and healthy, it's still worth running the comparison.

Laid off from Oracle? Get your real numbers in 5 minutes.

We'll put COBRA, ACA and a nationwide private PPO side by side for your exact situation — verify your doctors, check your prescriptions, and tell you straight which one wins. Free, no obligation.

Will you qualify for a private PPO?

Likely to qualify

- No major chronic conditions

- No hospitalizations in the last 2–3 years

- Few or no ongoing prescriptions

- No active or planned specialty care

- Non-smoker, or quit 12+ months ago

May not qualify

- Type 1 or Type 2 diabetes

- Cardiac history or active heart disease

- Active cancer or recent remission

- Multiple ongoing specialty medications

- Autoimmune conditions

If underwriting isn't a fit, that's a real answer and we'll say so — COBRA or the marketplace becomes the right path, and your layoff opens a Special Enrollment Period either way. We're an independent brokerage; the honest recommendation matters more to us than any single sale.

Related reading

- Amazon layoffs & COBRA: why it's too expensive and what to do instead

- Left your job? How to cut your COBRA bill in half

- Marketplace vs private PPO: an honest comparison

Frequently asked questions

How much does COBRA cost after an Oracle layoff?

It's whatever your Oracle plan actually costs, in full, plus up to a 2% administrative fee — not the payroll deduction you were used to seeing. Depending on your plan tier and how many people are on it, that commonly lands between roughly $600 and $1,800+ per month. Your COBRA election notice states your exact figure. If it looks high, that's not an error — it's the first time you're seeing the real price of the plan.

Does Oracle pay for any of my COBRA coverage?

Check your specific severance paperwork, because terms vary by package and by role. Some employers subsidize COBRA for a period; others don't. If yours doesn't include a COBRA subsidy, you're paying the full premium from day one — which is exactly when comparing alternatives is worth the twenty minutes.

How long do I have to decide?

60 days from the date you lost coverage, or from the date on your COBRA election notice, whichever is later. COBRA is retroactive within that window, so electing on day 55 still covers you from day one. Use the window — don't let it expire by default.

Can I leave COBRA later if I find something cheaper?

Yes. You can cancel COBRA at any time with no penalty and no minimum term. If you're approved for a private PPO or enroll in a marketplace plan, you cancel COBRA with the plan administrator and the new coverage takes over.

What if I get another job in a few months?

If your new employer offers group coverage, you enroll as a new hire and drop the private plan. Some people keep the private plan anyway if the new group plan is expensive or has a narrow network. Either way you're not locked in.

Will my doctors be covered?

We check your specific providers before you apply, not after. Nationwide PPO networks reach most physicians, specialists and hospital systems that accept PPO insurance — but we confirm yours by name so there are no surprises.

Compare COBRA vs private PPO with your actual numbers.

Most healthy people coming off a corporate plan are surprised how much comes off the monthly bill. We run the comparison and pre-screen your underwriting eligibility at no cost.

RKA Insurance Advisors is an independent insurance brokerage and is not affiliated with, endorsed by, or sponsored by Oracle Corporation. Oracle is a trademark of its respective owner and is referenced here solely for identification and news-commentary purposes. Workforce-reduction figures are as publicly reported. Severance and benefit terms vary by individual package — always review your own paperwork and plan documents.

Robert Adams * President & Licensed Agent * NPN 19540130 * Licensed in 30 states. Premium estimates are illustrative and based on general market data — actual premiums vary by age, state, health profile, and underwriting outcome. Private medically underwritten plans are not ACA-compliant and are subject to medical underwriting — not all applicants qualify. COBRA costs and timelines vary by employer plan. Consult your benefits administrator and a licensed advisor for your specific situation. This content is for informational purposes only and does not constitute insurance, legal, tax, or financial advice.