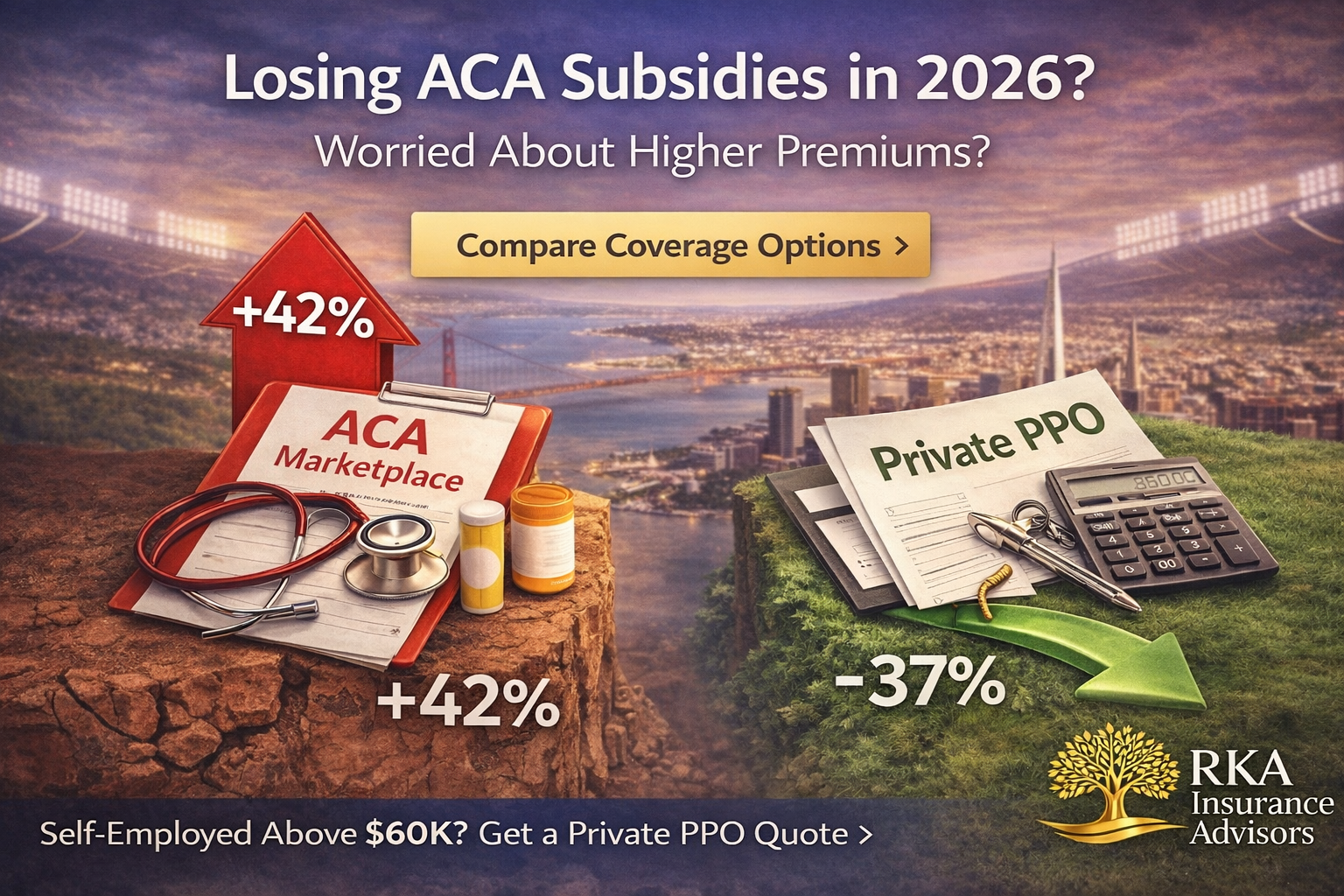

ACA Subsidy Cliff 2026: What Self-Employed Earners Above $60K Need to Know

Enhanced ACA subsidies expired December 31, 2025. If you earn above $60,240, you now pay the full unsubsidized Marketplace premium. Here's what changed — and what self-employed professionals in good health can do about it.

Private PPO * ACA 2026 * Self-Employed

ACA Subsidy Cliff 2026: What Self-Employed Earners Above $60K Need to Know

What changed in 2026

Before (2021-2025)

- Enhanced credits capped premiums at 8.5% of income

- Subsidies available at any income level

- Higher earners still got meaningful help

Now (2026)

- Subsidies cut off at $60,240 (individual)

- Above that - 100% full unsubsidized rate

- Full-price Silver plans average $600-$900/mo*

- Deductibles typically $4,000-$8,000

Marketplace vs Private PPO

- Guaranteed issue - no health screening

- Subsidies if income under $60,240

- Often HMO/EPO - referrals common

- Open enrollment window only

- Income reconciliation at tax time

- Full price if above subsidy threshold

- Health underwriting required

- Premiums based on health - not income

- Nationwide PPO access - no referrals

- Available any month - no enrollment window

- No subsidy reconciliation at tax time

- Can cost significantly less for healthy applicants*

Who Private PPO works best for

Income above $60K

- No subsidies available anyway

- Private PPO often cheaper

Variable income

- No mid-year reconciliation risk

- Fixed premium regardless of earnings

Missed open enrollment

- No qualifying event needed

- Coverage can start within days

How RKA helps

What we do

- Confirm your exact subsidy eligibility

- Verify your doctors in both ACA and PPO networks

- Project total annual cost - premium + deductible

- Pre-screen PPO eligibility before you apply

What you get

- Side-by-side ACA vs PPO comparison

- No surprises at application or tax time

- Coverage that fits your income and health

- A licensed advisor - not a call center

We verify your doctors, check your prescriptions, and compare ACA vs private PPO with real numbers. No pressure, no obligation.

Frequently Asked Questions

What is the ACA subsidy cliff in 2026?

The income point where premium tax credits phase out entirely - $60,240 for individuals in 2026. Earn $1 above that and you pay the full unsubsidized rate.

Are private PPO plans available if I missed open enrollment?

Yes. Private medically underwritten PPO plans are available year-round. No qualifying life event required.

How much could I save with a private PPO?

It depends on your age, state, and health history. For healthy applicants above the subsidy threshold, savings can be significant. We run the exact comparison for your situation at no cost.

What does medically underwritten mean?

The insurer reviews your health history before approving coverage. We pre-screen your eligibility so you know where you stand before submitting a full application.

Robert Adams * President & Licensed Agent * NPN 19540130 * Licensed in 30 states. For educational purposes only. *Premium estimates based on publicly available 2026 rate data and vary significantly by age, state, and plan. Speak to a licensed advisor for exact figures.

Open Enrollment Shock: 2026 Rates & Out-of-Pocket Costs Jump as Subsidy Enhancements Roll Back

2026 Marketplace health insurance rates are out—and they’re higher across the board. Premiums, deductibles, and maximum out-of-pocket costs are all climbing as enhanced subsidies roll back. See how these changes affect families heading into Open Enrollment and explore lower-cost Private PPO options.

Oct 30 • Written by Robert Adams

Open Enrollment Shock: 2026 Rates & Out-of-Pocket Costs Jump as Subsidy Enhancements Roll Back

Fast take: 2026 Marketplace premiums are up, maximum out-of-pocket limits increased, and enhanced subsidies are rolling back. A typical family of four (two 36-year-old adults + two kids) saw the lowest Bronze option jump from $1,267/mo in 2025 (OOP max $9,200) to $1,667/mo in 2026 (OOP max $10,000).

Open Enrollment is here. If you simply “let it renew,” you’ll likely pay more in 2026—often for less protection. Rate filings show across-the-board increases driven by medical inflation and policy changes. With the enhanced subsidies rolling back, many middle-income families now feel the full price pressure.

What changed for 2026

- Premiums: Double-digit increases are common across Bronze/Silver/Gold.

- Max out-of-pocket: Raised again for 2026 (example above: $9,200 → $10,000).

- Subsidy rollbacks: The expanded tax credits that softened 2024–2025 pricing are fading, raising net costs for many households.

Real-world snapshot (family of 4)

- 2025 lowest Bronze: $1,267/mo • Deductible $6,500 • OOP max $9,200.

- 2026 lowest Bronze: $1,667/mo • Deductible $7,500 • OOP max $10,000.

Same family, same metal tier—meaningfully higher monthly cost and higher exposure before the plan pays fully.

Don’t renew blind. We compare ACA vs. Private PPO side-by-side and confirm your doctors.

Moves to make now

- Price the real year: Premium + expected usage (copays/coinsurance) + deductible + OOP risk.

- Check doctors & meds: Verify network and formulary before you enroll.

- Compare ACA vs. Private PPO: If you qualify medically, PPOs can cut total cost and OOP exposure.

We’ll verify your doctors/prescriptions, model 2026 costs, and enroll you correctly—no pressure, just answers.

Quick FAQs

Will 2026 increases hit me immediately?

Yes—your 2026 premium and OOP limits apply based on your effective date. We’ll confirm your exact numbers.

Are Private PPOs available in my state?

Often, yes (underwriting required). We’ll pre-screen and confirm networks.

Can you confirm my doctors are in-network?

Yes. That’s step one before we quote anything.

For education only; eligibility, benefits, and availability vary by carrier and state. Always review official plan documents.

Robert Adams

RKA Insurance Advisors • Private & Marketplace Health Coverage

561-806-9913 •

info@RKAinsuranceadvisors.com •

Book an Appointment