Open Enrollment Shock: 2026 Rates & Out-of-Pocket Costs Jump as Subsidy Enhancements Roll Back

2026 Marketplace health insurance rates are out—and they’re higher across the board. Premiums, deductibles, and maximum out-of-pocket costs are all climbing as enhanced subsidies roll back. See how these changes affect families heading into Open Enrollment and explore lower-cost Private PPO options.

Oct 30 • Written by Robert Adams

Open Enrollment Shock: 2026 Rates & Out-of-Pocket Costs Jump as Subsidy Enhancements Roll Back

Fast take: 2026 Marketplace premiums are up, maximum out-of-pocket limits increased, and enhanced subsidies are rolling back. A typical family of four (two 36-year-old adults + two kids) saw the lowest Bronze option jump from $1,267/mo in 2025 (OOP max $9,200) to $1,667/mo in 2026 (OOP max $10,000).

Open Enrollment is here. If you simply “let it renew,” you’ll likely pay more in 2026—often for less protection. Rate filings show across-the-board increases driven by medical inflation and policy changes. With the enhanced subsidies rolling back, many middle-income families now feel the full price pressure.

What changed for 2026

- Premiums: Double-digit increases are common across Bronze/Silver/Gold.

- Max out-of-pocket: Raised again for 2026 (example above: $9,200 → $10,000).

- Subsidy rollbacks: The expanded tax credits that softened 2024–2025 pricing are fading, raising net costs for many households.

Real-world snapshot (family of 4)

- 2025 lowest Bronze: $1,267/mo • Deductible $6,500 • OOP max $9,200.

- 2026 lowest Bronze: $1,667/mo • Deductible $7,500 • OOP max $10,000.

Same family, same metal tier—meaningfully higher monthly cost and higher exposure before the plan pays fully.

Don’t renew blind. We compare ACA vs. Private PPO side-by-side and confirm your doctors.

Moves to make now

- Price the real year: Premium + expected usage (copays/coinsurance) + deductible + OOP risk.

- Check doctors & meds: Verify network and formulary before you enroll.

- Compare ACA vs. Private PPO: If you qualify medically, PPOs can cut total cost and OOP exposure.

We’ll verify your doctors/prescriptions, model 2026 costs, and enroll you correctly—no pressure, just answers.

Quick FAQs

Will 2026 increases hit me immediately?

Yes—your 2026 premium and OOP limits apply based on your effective date. We’ll confirm your exact numbers.

Are Private PPOs available in my state?

Often, yes (underwriting required). We’ll pre-screen and confirm networks.

Can you confirm my doctors are in-network?

Yes. That’s step one before we quote anything.

For education only; eligibility, benefits, and availability vary by carrier and state. Always review official plan documents.

Robert Adams

RKA Insurance Advisors • Private & Marketplace Health Coverage

561-806-9913 •

info@RKAinsuranceadvisors.com •

Book an Appointment

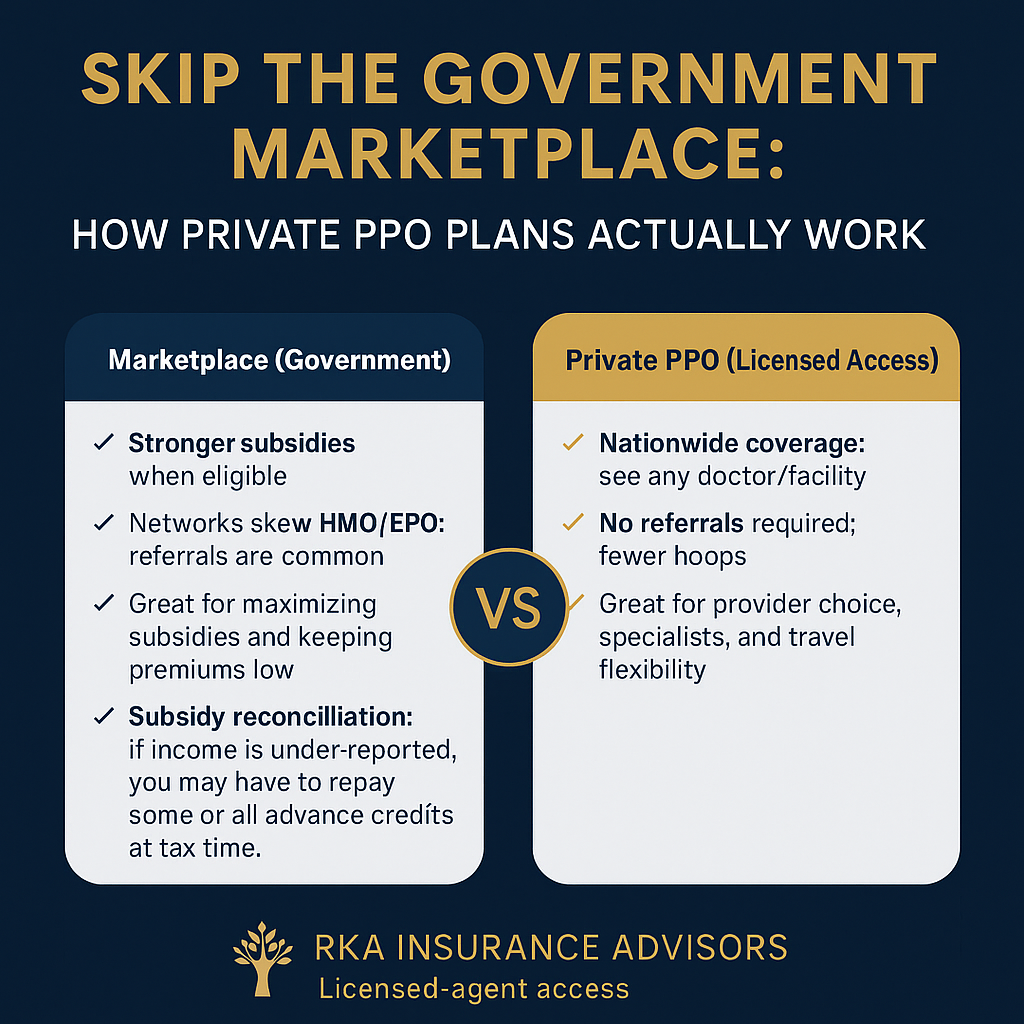

Skip the Government Marketplace: How Private PPO Plans Actually Work

Fast guide to non-Marketplace Private PPOs—how they bill, who they fit, and what to verify first. We’ll confirm your doctors, compare options, and show clear costs.

Skip the Government Marketplace: How Private PPO Plans Actually Work

Prefer private, licensed-access coverage? Here’s the fast, practical guide—what it is, how it bills, and how to check if it fits your doctors, travel, and budget.

Why some people skip the Marketplace

- Keep specific doctors/hospitals. Many Marketplace options are HMO/EPO with referrals.

- Travel flexibility. Want nationwide, not just local networks.

- Fewer gatekeepers. Prefer no referrals for specialists or imaging.

- Income too high for meaningful subsidies—or you don’t want tax-credit involvement.

- If your income qualifies, Marketplace can be the cheapest route.

- Credits reconcile on your tax return; under-reporting income can create payback.

- Private PPOs skip subsidies entirely—pricing is based on age, ZIP, benefits, and network.

How Private PPO actually works

- Nationwide PPO access in eligible networks—keep your specialists and preferred hospitals.

- No referrals for specialists (typical), fewer hoops to schedule care.

- Enroll through a licensed agent; options vary by state and carrier.

- Premiums aren’t tied to ACA income credits.

- Your exact doctors and facilities are in-network (we check for you).

- Copays vs coinsurance on high-ticket items (imaging, outpatient surgery).

- Prescription tiers and any prior-auth on key meds.

- Out-of-pocket maximum is a number you can live with.

What drives price (non-subsidized)

The big levers

- Age rating for adults; kids usually add less than another adult.

- ZIP/county + network breadth.

- Deductibles, coinsurance, copays, and the out-of-pocket max.

Ways to keep it efficient

- Don’t overbuy—match benefits to how you actually use care.

- Choose networks that include your real providers (not just brand names).

- Use generics when clinically appropriate; we’ll check formulary tiers.

Who typically chooses Private PPO

Strong fit

- Self-employed/1099 families who want broad doctor choice.

- Frequent travelers or multi-state households.

- People who dislike referral bottlenecks.

Maybe not a fit

- Households whose main goal is max subsidies and the lowest possible premium.

- Anyone who does not have specific providers to keep and rarely needs out-of-area care.

Want the best non-Marketplace fit in your ZIP?

We’ll verify your doctors and meds, compare PPO options, and show clear costs. No pressure—just answers.

FAQ

Are Private PPOs the same as Marketplace plans?

Do Private PPOs need referrals?

Will I owe taxes if I’m not using subsidies?

How do I know if my doctor is covered?

How do we start?

This overview is educational, not tax or legal advice. Plan availability and rules vary by state and carrier. Eligibility and enrollment subject to underwriting/plan terms where applicable.