COBRA Is Expensive. Here's the Private PPO Alternative

COBRA coverage after job loss can cost significantly more than you expect — you're now paying 100% of the premium with no employer subsidy. For healthy applicants, a private underwritten PPO is often a lower-cost alternative with no open enrollment restrictions.

Private PPO • COBRA Alternative • Self-Employed

COBRA Is Expensive. Here's the Private PPO Alternative

Why COBRA costs so much

When you're employed, your employer typically covers a significant portion of your health insurance premium — often 70–80% of the cost. You only see your small share in your paycheck. When you leave that job and elect COBRA, you suddenly become responsible for the entire premium — your share plus your employer's share — plus an administrative fee.

For individual coverage, COBRA costs can be a significant monthly expense. For family coverage, it can be considerably more. Most people are shocked by the amount when they see their COBRA election notice.

COBRA vs Private PPO

- Keeps your existing coverage and doctors

- No health screening required

- Retroactive — can elect after a gap

- You pay full employer + employee premium

- Plus up to 2% administrative fee

- Limited to 18 months in most cases

- Expensive for most healthy individuals

- Underwritten based on your health

- Healthy applicants often pay significantly less

- Nationwide PPO access — no referrals

- Lower deductible options — including $0 deductible plans

- Available any month — no enrollment window

- No time limit on coverage

When COBRA makes sense vs when to switch

COBRA may be better if...

- You have ongoing treatment in progress

- You're mid-year with a deductible nearly met

- You have a health condition that affects PPO eligibility

- You need continuity with specific doctors

Private PPO may be better if...

- You're healthy with no active conditions

- COBRA cost is a significant financial burden

- You want long-term coverage, not just 18 months

- You want nationwide PPO access going forward

How RKA helps

What we do

- Compare your COBRA cost vs private PPO options

- Pre-screen your PPO eligibility

- Verify your doctors are in the new network

- Help you time the transition correctly

What you get

- An honest side-by-side cost comparison

- Coverage that doesn't expire in 18 months

- No income reporting or reconciliation

- A licensed advisor — not a call center

We run the numbers for your specific situation. Most healthy applicants are surprised at the difference. No pressure, no obligation.

Frequently Asked Questions

Is private PPO cheaper than COBRA?

For healthy applicants, private PPO plans are frequently significantly less expensive than COBRA. COBRA requires you to pay the full group premium including the portion your employer was covering. Private PPO premiums are based on your individual health profile.

Can I switch from COBRA to a private PPO any time?

Yes. You can leave COBRA and switch to a private PPO at any time. Private PPO plans are available year-round with no enrollment window.

What if I have a health condition and can't get private PPO?

If you don't qualify for private underwriting, COBRA may be the right choice — especially if you have ongoing treatment or a deductible nearly met. ACA Special Enrollment may also apply if you've recently lost employer coverage.

How long does COBRA coverage last?

In most cases, COBRA coverage lasts 18 months. Some situations — such as disability — may extend it to 29 or 36 months. Private PPO plans have no such time limit.

Robert Adams * President & Licensed Agent * NPN 19540130 * Licensed in 32 states. For educational purposes only. *Premium estimates vary significantly by age, state, health history, and plan. Speak to a licensed advisor for exact figures.

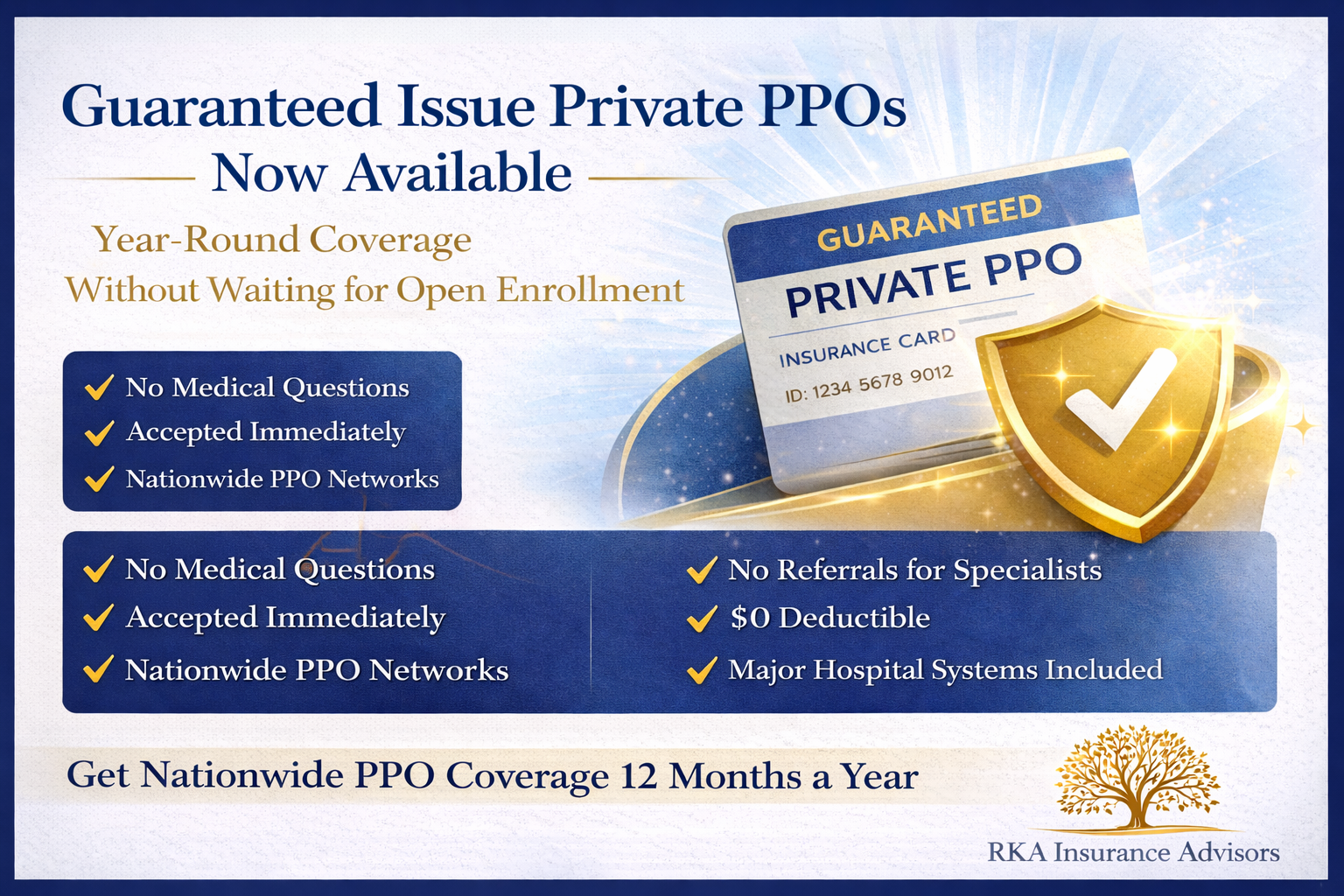

Guarantee Issue Private PPOs: Year-Round Coverage Without Medical Underwriting | RKA

Guarantee issue private PPOs now available in select markets—year-round enrollment, nationwide networks, no medical underwriting required. Perfect if you missed Open Enrollment or need coverage with pre-existing conditions. We check availability in your ZIP.

Guarantee Issue Private PPOs Now Available – Year-Round Coverage Without Waiting for Open Enrollment

Fast take: New guarantee issue private PPO options are available in select markets—year-round enrollment, broad nationwide networks, and no medical underwriting required. If you need coverage outside Open Enrollment and don't have a Special Enrollment Period, this may be your path. We'll verify providers and show clear costs before you commit.

Need coverage now without waiting for Open Enrollment?

We'll confirm if guarantee issue PPOs are available in your ZIP, verify your doctors, and enroll you quickly.

Get Free Quotes Book a CallWhat makes guarantee issue PPOs different

For years, private PPO plans required medical underwriting—health questions that could result in denial or exclusions if you had pre-existing conditions. Guarantee issue private PPOs solve this problem by combining the best features of ACA Marketplace plans (no medical questions, guaranteed acceptance) with the advantages of private PPO networks (broader access, fewer restrictions, year-round availability).

Guarantee Issue

✓ No medical questions

✓ No health exams

✓ Cannot be denied

✓ Pre-existing conditions covered

✓ Coverage starts immediately

PPO Network Benefits

✓ Nationwide provider access

✓ No referrals for specialists

✓ Out-of-network coverage

✓ Major hospital systems included

✓ Travel-friendly coverage

Year-round enrollment

These plans are available outside the standard November-January Open Enrollment period. You can apply and start coverage any month of the year without needing a Qualifying Life Event.

Perfect if you:

✓ Missed the January 15 deadline

✓ Don't have a qualifying life event

✓ Need coverage immediately

✓ COBRA is too expensive

✓ Want to switch plans mid-year

Great for:

✓ Frequent travelers

✓ Multi-state households

✓ Specific doctor requirements

✓ Higher income (no subsidies)

✓ Pre-existing conditions

How guarantee issue PPOs compare

| Feature | Guarantee Issue PPO | ACA Marketplace | Underwritten PPO |

|---|---|---|---|

| Medical questions | None | None | Yes (can deny) |

| Enrollment window | Year-round | Open Enrollment only | Year-round (if approved) |

| Network type | Nationwide PPO | Often HMO/EPO | Nationwide PPO |

| Subsidies | No | Yes (if eligible) | No |

| Pre-existing conditions | May have exclusions & limits | Covered day 1 | Covered if approved & disclosed |

Simple next steps

1. Check availability

Not offered in all states or ZIP codes. We'll confirm immediately if these plans are available in your area.

2. Verify providers

Send your doctor list. We'll check network participation before you commit—even PPOs don't cover every provider.

3. Compare costs

We'll show total annual cost: premiums + deductibles + expected usage across all your options.

4. Enroll fast

Most plans start on the 1st or 15th of the month. We'll time your application to avoid coverage gaps.

Quick FAQs

Are guarantee issue PPOs available in all states?

No—availability varies by carrier and market. We'll check your specific ZIP code and confirm which options exist in your area.

How do premiums compare to Marketplace plans?

Often similar to unsubsidized Marketplace plans, but with PPO flexibility instead of HMO/EPO restrictions. If you qualify for Marketplace subsidies, the subsidized plan will almost always be cheaper.

Can I switch from a Marketplace plan to a guarantee issue PPO mid-year?

Yes, if you're willing to give up subsidies (if you have them). We'll compare total costs—including lost subsidies—before you make the switch to ensure it makes financial sense.

What if I have a serious pre-existing condition?

Guarantee issue means exactly that—no one can be turned down. Pre-existing conditions may have wait periods or exclusions.

For education only; availability and benefits vary by carrier, state, and ZIP code. Always review official plan documents.