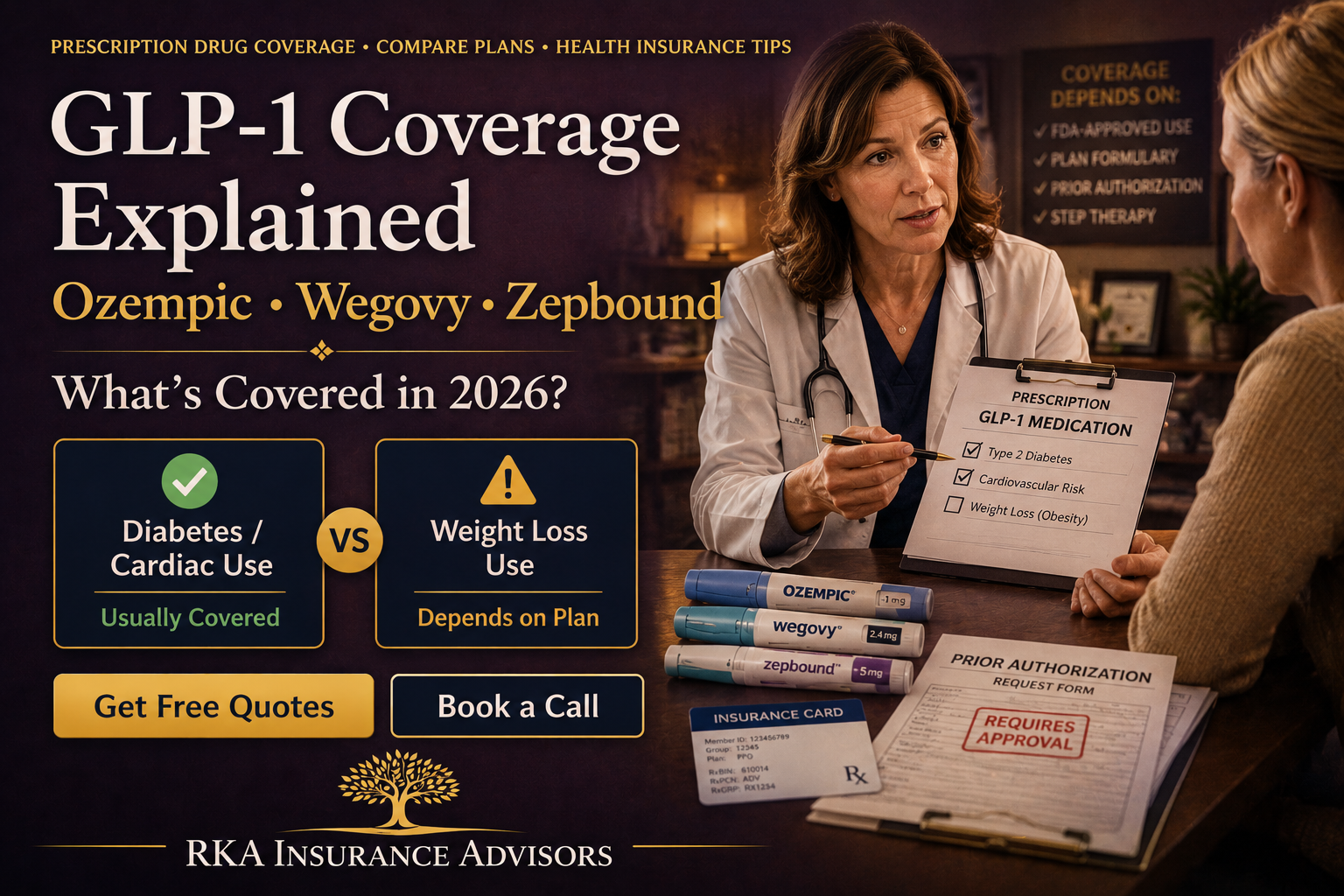

GLP-1 Coverage Explained: Ozempic, Wegovy & Zepbound in 2026

Whether a plan covers a GLP-1 usually comes down to what it's prescribed for. Diabetes use is commonly covered; weight-loss coverage in 2026 is limited, shrinking, and almost always tied to prior authorization. Here's how each coverage path works — and what to check before you enroll.

Prescription Drug Coverage • Compare Plans • Health Insurance Tips

GLP-1 Coverage Explained: Ozempic, Wegovy & Zepbound in 2026

First, what counts as a "GLP-1"?

GLP-1 receptor agonists mimic a hormone that helps regulate blood sugar and appetite. The brand names get used interchangeably in the headlines, but the FDA approvals behind them are different — and that difference drives whether your plan pays.

Approved for type 2 diabetes

- Ozempic (semaglutide)

- Mounjaro (tirzepatide)

- Rybelsus (oral semaglutide)

- Trulicity, Victoza

Approved for chronic weight management

- Wegovy (semaglutide)

- Zepbound (tirzepatide)

- Saxenda (liraglutide)

The 2026 coverage picture, by plan type

| Coverage path | For diabetes / cardiac use | For weight loss alone |

|---|---|---|

| ACA Marketplace plans | Commonly covered, often with restrictions | Rarely covered — and declining |

| Employer plans | Commonly covered | Only if the employer buys a weight-management rider |

| Private PPO plans | Varies by formulary — verify the drug list | Often excluded or on a high specialty tier |

| Medicare Part D | Covered for approved non-weight uses | Limited — see the GLP-1 Bridge note below |

Why weight-loss coverage keeps shrinking

At roughly $1,000+ per month at list price, GLP-1s have become one of the fastest-growing line items in pharmacy budgets — and insurers have pointed to them as a factor pushing 2026 marketplace premiums higher. The result: many carriers have narrowed weight-loss coverage to diabetes-only, added prior authorization, or dropped it entirely for individual and small-group members effective January 2026.

What this means for you

- A plan covering Ozempic for diabetes may not cover Wegovy for weight loss.

- Even "covered" weight-loss prescriptions usually need prior authorization first.

- Coverage can change at renewal — what's on the formulary this year may shift next year.

If a plan does cover it: how approval usually works

When a plan includes weight-loss GLP-1s, approval criteria tend to mirror the FDA prescribing guidelines:

Typical approval requirements

- BMI of 30+, or 27+ with a weight-related condition (high blood pressure, prediabetes, high cholesterol)

- A documented diagnosis with the correct code from your provider

- A prior authorization request submitted by your prescriber

- In some plans, step therapy — trying a lower-cost option first

Good to know

- Prior authorization can take up to 10 business days

- Ask your prescriber's office to submit it the day the script is written

- Denials can be appealed — and appeals succeed more often than people expect

If your plan excludes it: lower-cost paths

A coverage denial isn't a dead end. Several manufacturer and pharmacy programs exist for people paying out of pocket:

Manufacturer direct

- NovoCare (Wegovy): injection from about $199/month for new patients, then higher; Wegovy pill from about $149/month

- LillyDirect (Zepbound): from about $299/month depending on dose

Pharmacy savings

- GoodRx and similar tools for semaglutide and tirzepatide pricing

- Commercial-insurance copay cards

- Manufacturer cards exclude government plans (Medicare/Medicaid)

A new Medicare GLP-1 Bridge program begins July 1, 2026, giving eligible Part D beneficiaries access to certain weight-loss GLP-1s for a $50 monthly copay through the end of 2027, with prior authorization and clinical criteria required. This applies to Medicare members specifically — separate from the under-65 coverage this guide focuses on.

What to check before you enroll in any plan

- Pull the plan's drug formulary and search the exact brand you take

- Review the Summary of Benefits and Coverage (SBC) — every plan must provide one

- Confirm the tier and whether prior authorization or step therapy applies

- Check whether coverage is tied to a diabetes diagnosis or includes weight management

Where we come in

- We'll run this formulary check with you before you commit to a plan

- Compare your options side by side across carriers

- No surprises at the pharmacy counter

- Free, and no obligation

We'll review the drug lists with you and compare your options side by side — at no cost.

Frequently Asked Questions

Is Ozempic covered by health insurance?

Ozempic is FDA-approved for type 2 diabetes (and cardiovascular risk reduction in certain adults with diabetes), so it's commonly covered when prescribed for those uses — often with prior authorization. It is not FDA-approved as a weight-loss drug, so plans generally won't cover it for weight loss alone.

Why would my plan cover Ozempic but not Wegovy?

They share the same active ingredient (semaglutide) but have different FDA approvals. Ozempic is approved for diabetes; Wegovy is approved for weight management. Formularies follow the approved use, so a plan can include one and exclude the other.

Do ACA Marketplace plans cover GLP-1s for weight loss?

Rarely in 2026. Industry analyses found only about 26 of roughly 300 marketplace carriers cover GLP-1s for obesity, concentrated in nine states, and coverage has been declining. Plans that do cover them typically require prior authorization or quantity limits. Always check the specific plan's formulary.

What if my prescription is denied?

Denials can often be appealed, and appeals succeed more often than people expect — many simply never file one. You can also use manufacturer direct programs and pharmacy savings tools while you sort out coverage. Your prescriber's office handles the prior authorization and appeal paperwork.

Can a private PPO plan get me GLP-1 coverage?

It depends entirely on the individual plan's formulary. Private PPO drug lists vary, and weight-loss GLP-1s are often excluded or placed on a high specialty tier. The reliable move is to verify the exact medication on the formulary before you enroll — which is something we can do with you directly.

We're an independent broker. We'll check the formulary, compare carriers, and tell you honestly what each plan covers for your situation. No pressure, no obligation.

Robert Adams * President & Licensed Agent * NPN 19540130 * Licensed in 30 states. This content is for informational purposes only and does not constitute insurance, medical, legal, tax, or financial advice. Prescription coverage, formularies, prior-authorization rules, and manufacturer program pricing vary by plan, state, and date and change frequently — verify details against your plan's current formulary and Summary of Benefits and Coverage, and consult your healthcare provider about any medication. Private medically underwritten plans are not ACA-compliant and are subject to medical underwriting — not all applicants qualify.