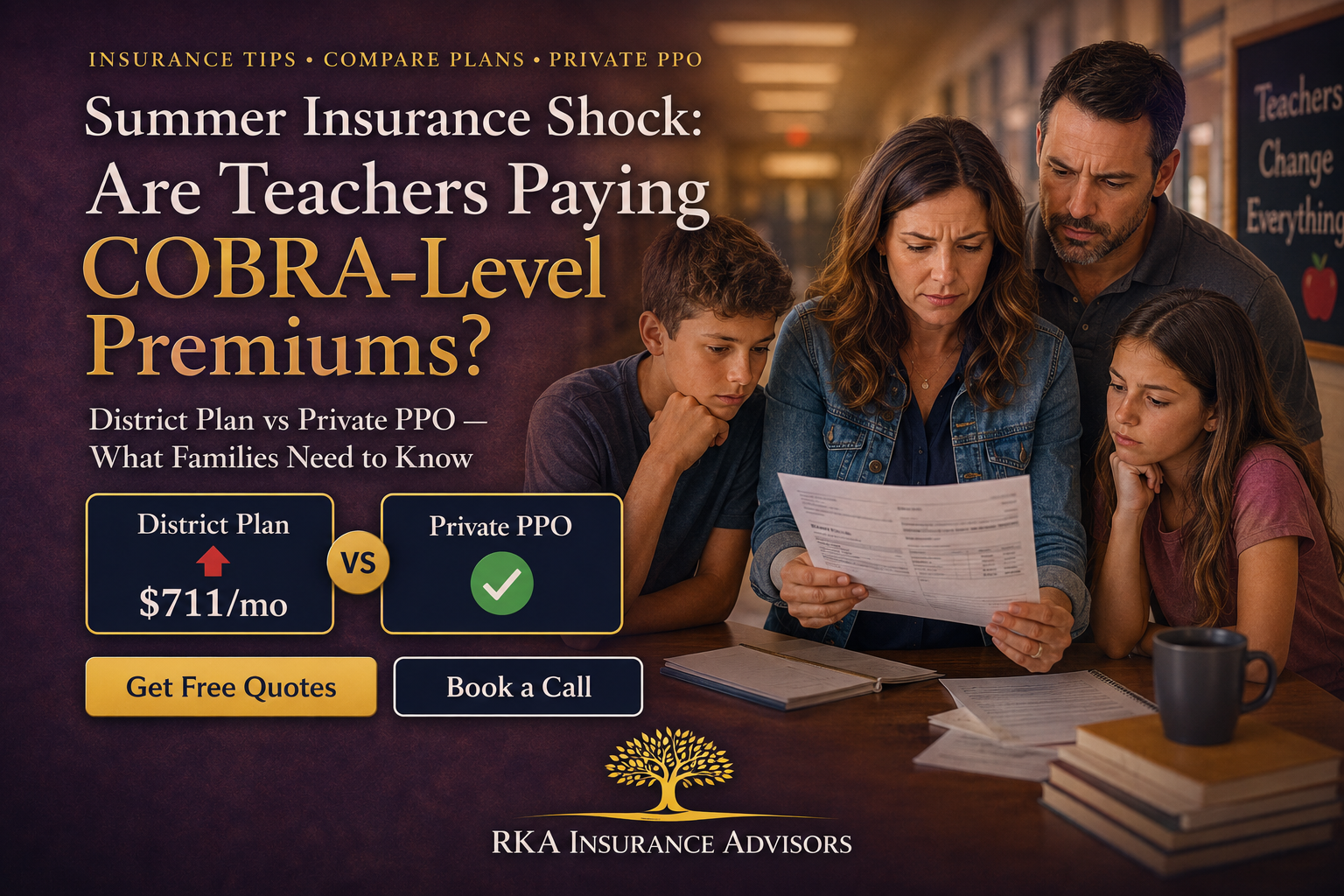

Summer Insurance Shock: Are Teachers Paying COBRA-Level Premiums?

Many teachers assume their "district health insurance" is a great deal — but family premiums often rival COBRA costs. For healthy families, moving dependents to a private PPO while keeping the teacher on the district plan can save $500–800/month

insurance Tips • Compare Plans • Private PPO

Summer Insurance Shock: Are Teachers Paying COBRA-Level Premiums?

The hidden cost of "district insurance"

Most teachers know their district contributes toward health insurance. What many don't realize is how that contribution is structured — and how little of it applies to family coverage.

According to the National Council on Teacher Quality (NCTQ), districts cover an average of 84% of employee-only premiums but only 64% of family premiums. The gap between those two numbers is where teachers get hit.

The result: a teacher paying $162/month for single coverage might pay $711/month or more for family coverage — a jump that rivals what they'd pay on COBRA.

Why family premiums are so high

Employee-only coverage

- District pays 80–90% of premium

- Teacher pays $100–200/month

- Feels like a "great benefit"

Family coverage

- District contribution doesn't scale proportionally

- Teacher picks up most of the dependent cost

- $600–900+/month is common

- Some districts exceed $1,000/month

In Texas specifically, the state contributes just $75/month toward employee coverage, plus a $150/month district minimum. That's $225/month total — for the teacher only. Family members? That's on you.

The split coverage strategy

Here's what some teachers are doing instead: keep the employee on the district plan (to capture the employer contribution), and move spouse and kids to a private medically underwritten PPO.

- Teacher stays on district plan — low cost, good coverage

- Dependents move to private PPO — often $400–600/month for spouse + kids

- Total family cost drops by $500–800/month in many cases

- Private plan has nationwide PPO network (UHC Choice Plus)

- No enrollment window — available any month

- Before: $780/month (district family plan)

- After — Teacher: $19/month (district employee-only)

- After — Spouse + 2 kids: $521/month (private PPO)

- New total: $540/month

- Savings: $240/month ($2,880/year)

Who this works for — and who it doesn't

Good candidates for split coverage

- Healthy spouse and children

- No major chronic conditions or ongoing specialty care

- Family members rarely use the healthcare system

- Current family premium exceeds $600/month

Not a fit if

- Spouse or child has significant health history

- Pre-existing conditions that require ongoing care

- Mental health or substance abuse treatment is needed

- You need guaranteed-issue coverage regardless of health

What private PPO coverage looks like

UnitedHealthcare Choice Plus PPO — Secure Advantage

- $0 day-to-day deductible — benefits start immediately

- 6 prepaid doctor visits per person/year

- $10 generic / $40 brand prescriptions

- Unlimited telehealth included

- $2,500–$10,000 deductible options for major medical

- 80/20 coinsurance up to max out-of-pocket

- Guaranteed renewable to age 65

What's not covered

- Inpatient mental health treatment

- Drug and alcohol rehabilitation

- Pre-existing conditions (underwriting required)

If these exclusions are a concern, district or ACA marketplace coverage may be the better path.

We'll compare your district family plan vs. employee-only + private PPO for dependents — and tell you honestly which path saves more.

How to know if this makes sense for you

Step 1 — Check your current family premium

- Look at your district benefits statement

- What are you actually paying for employee + dependents?

- Is your total above $600/month?

Step 2 — Get a private quote for dependents

- We'll run numbers for spouse and kids on a private PPO

- Based on their ages, ZIP code, and health profile

- Takes about 5 minutes

Step 3 — Compare total costs

- District employee-only + private PPO for dependents

- vs. district family plan

- The math tells you whether it's worth it

Step 4 — Pre-screen for underwriting

- Before applying, we check whether your family members are likely to qualify

- No surprises

- Honest assessment before you commit

Frequently Asked Questions

Does this work during the school year or only in summer?

Private PPO plans are available any month — no enrollment window. You can make the switch whenever your district's open enrollment allows you to drop dependents from the district plan.

What if my district requires me to cover my spouse?

Most districts don't require dependent coverage — it's optional. Check your benefits handbook or HR department. If coverage is truly required, this strategy won't work.

Can I add my kids back to the district plan later if needed?

Typically yes — during the next open enrollment period, or if you have a qualifying life event (job loss, birth, etc.). Confirm with your district's HR.

What if my spouse doesn't qualify for private coverage?

If underwriting isn't available for your spouse due to health history, they can stay on the district plan or explore ACA marketplace options. We compare all paths honestly.

Does this affect my pension or retirement benefits?

No. Your employment status and pension contributions are separate from which health plan your dependents use.

The bottom line

Not every teacher is overpaying for family coverage — but many are. If your district family premium is $600/month or more and your dependents are healthy, it's worth running the numbers on a split coverage strategy.

We'll compare your district family plan vs. employee-only + private PPO for dependents — and tell you honestly which makes sense.

Get a free comparison — your district plan vs. private PPO options for your family.

Robert Adams * President & Licensed Agent * NPN 19540130 * Licensed in 32 states. Premium estimates are illustrative and based on general market data — actual premiums vary by age, state, health profile, and underwriting outcome. Private medically underwritten plans are not ACA-compliant and are subject to medical underwriting — not all applicants qualify. District plan costs vary significantly by state and district. This content is for informational purposes only and does not constitute insurance, legal, tax, or financial advice.