Why PPOs Are King: The Case for Nationwide Networks and Provider Freedom

Why PPOs beat HMOs for self-employed professionals, business owners, and frequent travelers: nationwide networks, no primary care gatekeepers, direct specialist access, and fewer authorization delays.

Why PPOs Are King: The Case for Nationwide Networks and Provider Freedom

Fast take: If you're self-employed, travel for work, or value direct access to specialists without referral red tape, PPO networks offer unmatched flexibility. No primary care gatekeepers, no waiting weeks for authorization, and coverage that works wherever you are—not just in your home county.

Tired of narrow HMO networks and referral requirements?

We'll show you nationwide PPO options and verify your doctors are covered—no restrictions, no runarounds.

Get Free Quotes Book a CallWhat makes PPO networks different

HMO/EPO (Most Marketplace plans)

✗ Primary care doctor required (PCP)

✗ Referrals needed for specialists

✗ Limited to local network only

✗ Out-of-network = not covered (except emergencies)

✗ Authorization delays common

PPO (Preferred Provider Organization)

✓ No primary care gatekeeper required

✓ See specialists directly—no referrals

✓ Nationwide network coverage

✓ Out-of-network benefits available

✓ Fewer authorization requirements

Who benefits most from PPO networks

Business owners & entrepreneurs

✓ Client meetings across multiple states

✓ Need care wherever business takes you

✓ Can't afford delays waiting for referrals

✓ Want specialist access without bureaucracy

Frequent travelers

✓ Snowbirds splitting time between states

✓ Digital nomads working remotely

✓ Families with second homes

✓ Need consistent coverage anywhere

People with specific provider needs

✓ Established relationship with specialist

✓ Prefer specific hospitals or facilities

✓ Need access to top-tier medical centers

✓ Don't want to change doctors

High-income households

✓ Don't qualify for meaningful ACA subsidies

✓ Paying full price either way

✓ Want maximum flexibility and choice

✓ Prefer premium networks and providers

Real-world scenarios where PPOs win

Scenario 1: The entrepreneur in pain

HMO path: Back pain → see PCP first → wait for referral → wait for specialist appointment → weeks of delays

PPO path: Back pain → call orthopedist directly → appointment this week → faster treatment

Scenario 2: The traveling consultant

HMO path: Urgent care needed in Dallas → not in network → pay full cost out-of-pocket → file claim, hope for reimbursement

PPO path: Urgent care in Dallas → nationwide network → normal copay → done

Scenario 3: The specialist relationship

HMO path: Your cardiologist isn't in network → forced to switch doctors → rebuild relationship from scratch

PPO path: Your cardiologist is in nationwide PPO → keep your doctor → continuity of care

Scenario 4: The imaging authorization

HMO path: Doctor orders MRI → need authorization → wait 5-7 business days → delay diagnosis

PPO path: Doctor orders MRI → schedule immediately → faster diagnosis and treatment

The hidden costs of HMO restrictions

Many people choose HMOs to save on monthly premiums, but the total cost equation includes more than just what you pay each month:

Time costs

✗ Waiting for PCP appointments before specialist referrals

✗ Authorization delays (5-7 days common for imaging/procedures)

✗ Extended treatment timelines due to referral requirements

✗ Lost productivity from delayed care

Out-of-pocket surprise costs

✗ Traveling for work? Out-of-network urgent care = full cost

✗ Emergency room in another state = potential balance billing

✗ Preferred specialist not in network = start over with new doctor

✗ Lab work at non-contracted facility = surprise bills

PPO networks for self-employed professionals

If you're self-employed, your health insurance needs are different from W-2 employees:

You can't afford downtime

No paid sick leave. Every day you're delayed waiting for referrals or authorizations is lost income. PPOs let you see specialists immediately and get treatment faster.

Your work location varies

Client sites, conferences, remote work from different states—you need coverage that travels with you, not just in your home county.

You control your own schedule

Don't waste time scheduling PCP visits just to get a referral. See the specialist directly and get back to work.

You're paying full freight anyway

If you don't qualify for subsidies, you're paying full price for ACA plans. PPO premiums are often comparable with far better access.

Common PPO myths debunked

❌ Myth: PPOs are always more expensive

Reality: For healthy applicants who don't qualify for subsidies, private underwritten PPOs often cost less than unsubsidized ACA plans—with better networks and lower deductibles.

❌ Myth: You don't need nationwide coverage

Reality: Even if you rarely travel, emergencies happen. Car accident on vacation? Family emergency out of state? Nationwide PPO coverage eliminates surprise bills.

❌ Myth: Referrals aren't a big deal

Reality: Referral requirements add 1-3 weeks to every specialist visit. For time-sensitive issues or busy professionals, this delay is costly.

❌ Myth: All PPOs are the same

Reality: PPO network size varies dramatically. We verify your specific doctors are in-network before you enroll—not all "nationwide" PPOs include every provider.

When to choose PPO over HMO/EPO

Choose PPO if...

✓ You're self-employed or own a business

✓ You travel frequently for work or personal reasons

✓ You have established relationships with specialists

✓ You don't qualify for meaningful ACA subsidies

✓ You value direct access without referral delays

✓ Time is money and you can't afford bureaucratic delays

HMO/EPO might work if...

✓ You qualify for strong ACA subsidies

✓ All your doctors are in a local HMO network

✓ You rarely travel and don't need out-of-area care

✓ You're comfortable with PCP gatekeeping

✓ You don't mind waiting for referrals and authorizations

✓ Lowest monthly premium is your only priority

How RKA finds the right PPO for you

Doctor verification first

We check your specific doctors, specialists, and hospitals against actual PPO networks—not just "find-a-doc" directories that are often outdated.

Multi-state coverage mapping

Travel between Florida and New York? We verify both locations have strong network coverage before you commit.

Total cost comparison

We model premiums + deductibles + expected usage for HMO vs PPO options—sometimes PPO costs less when you factor in out-of-network exposure.

Private vs Marketplace PPO options

Marketplace has limited PPO options. We compare against private underwritten PPOs that may offer better networks and lower deductibles.

Ready for nationwide PPO freedom?

We'll verify your doctors, compare PPO options, and show you total costs—no referral requirements, no network restrictions.

Get Free Quotes Book a CallQuick FAQs

Are PPOs available on the ACA Marketplace?

Some states offer limited PPO options on the Marketplace, but many areas only have HMO/EPO plans. Private underwritten PPOs (off-exchange) often offer broader networks and better benefits for healthy applicants.

Do PPOs really cost that much more than HMOs?

For subsidized plans, yes. But if you don't qualify for subsidies, private PPO premiums are often comparable to unsubsidized HMO/EPO plans—with far better access and lower deductibles.

What does "nationwide PPO" actually mean?

Network coverage in all 50 states (or most states). Specific provider availability varies—we verify your doctors are included, not just that the network exists in your state.

Can I switch from HMO to PPO mid-year?

ACA plans can only switch during Open Enrollment (or with a qualifying event). Private PPOs are available year-round if you qualify for underwriting.

For education only; network access and benefits vary by carrier and state. Always verify providers before enrollment. Eligibility for private underwritten plans subject to medical underwriting.

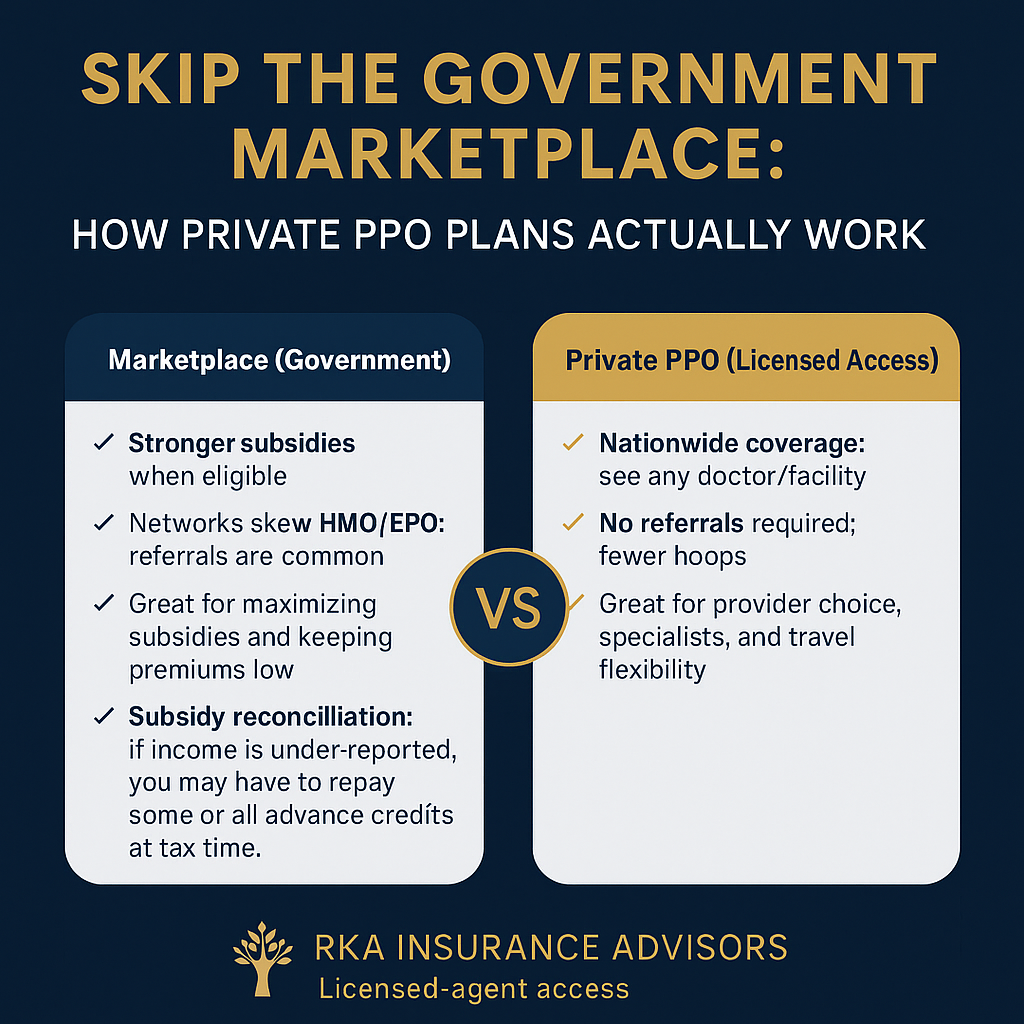

Skip the Government Marketplace: How Private PPO Plans Actually Work

Fast guide to non-Marketplace Private PPOs—how they bill, who they fit, and what to verify first. We’ll confirm your doctors, compare options, and show clear costs.

Skip the Government Marketplace: How Private PPO Plans Actually Work

Prefer private, licensed-access coverage? Here’s the fast, practical guide—what it is, how it bills, and how to check if it fits your doctors, travel, and budget.

Why some people skip the Marketplace

- Keep specific doctors/hospitals. Many Marketplace options are HMO/EPO with referrals.

- Travel flexibility. Want nationwide, not just local networks.

- Fewer gatekeepers. Prefer no referrals for specialists or imaging.

- Income too high for meaningful subsidies—or you don’t want tax-credit involvement.

- If your income qualifies, Marketplace can be the cheapest route.

- Credits reconcile on your tax return; under-reporting income can create payback.

- Private PPOs skip subsidies entirely—pricing is based on age, ZIP, benefits, and network.

How Private PPO actually works

- Nationwide PPO access in eligible networks—keep your specialists and preferred hospitals.

- No referrals for specialists (typical), fewer hoops to schedule care.

- Enroll through a licensed agent; options vary by state and carrier.

- Premiums aren’t tied to ACA income credits.

- Your exact doctors and facilities are in-network (we check for you).

- Copays vs coinsurance on high-ticket items (imaging, outpatient surgery).

- Prescription tiers and any prior-auth on key meds.

- Out-of-pocket maximum is a number you can live with.

What drives price (non-subsidized)

The big levers

- Age rating for adults; kids usually add less than another adult.

- ZIP/county + network breadth.

- Deductibles, coinsurance, copays, and the out-of-pocket max.

Ways to keep it efficient

- Don’t overbuy—match benefits to how you actually use care.

- Choose networks that include your real providers (not just brand names).

- Use generics when clinically appropriate; we’ll check formulary tiers.

Who typically chooses Private PPO

Strong fit

- Self-employed/1099 families who want broad doctor choice.

- Frequent travelers or multi-state households.

- People who dislike referral bottlenecks.

Maybe not a fit

- Households whose main goal is max subsidies and the lowest possible premium.

- Anyone who does not have specific providers to keep and rarely needs out-of-area care.

Want the best non-Marketplace fit in your ZIP?

We’ll verify your doctors and meds, compare PPO options, and show clear costs. No pressure—just answers.

FAQ

Are Private PPOs the same as Marketplace plans?

Do Private PPOs need referrals?

Will I owe taxes if I’m not using subsidies?

How do I know if my doctor is covered?

How do we start?

This overview is educational, not tax or legal advice. Plan availability and rules vary by state and carrier. Eligibility and enrollment subject to underwriting/plan terms where applicable.

Telemedicine Benefits: Save Time, Cut Costs, and Skip the Waiting Room | RKA Insurance Advisors

See a clinician by phone or video—often at $0 copay. When telemedicine works best, what’s covered, and how to get plans with $0 virtual visits.

Health Guides • Updated • Written by Robert Adams

Telemedicine Benefits: Faster Care, Lower Cost, Less Hassle

Fast take:

Telemedicine lets you meet with board-certified clinicians by phone or video, usually in minutes. It’s great for common issues, refills, and follow-ups—often at $0 copay on many plans. You save time, avoid waiting rooms, and cut costs without sacrificing quality.

- • See a clinician from home, work, or travel—no waiting room.

- • Perfect for minor illnesses, refills, and quick follow-ups.

- • Visits typically run ~15 minutes.

- • Fewer germ exposures vs. urgent care/ER waiting areas.

- • Helpful for immunocompromised, pregnant, and elderly.

- • Triage contagious symptoms before in-person care.

- • Family, internal, and pediatrics: easy follow-ups and check-ins.

- • Manage hypertension, diabetes, asthma, mental health, more.

- • Many platforms offer 24/7 access.

- • Many plans cover telehealth at $0 or low copay.

- • Cash-pay telehealth is typically cheaper than in-office rates.

- • Using telehealth for non-emergencies avoids costly ER bills.

Good uses vs. go in-person

Use telemedicine for

- Cold/flu, sore throat, sinus/ear issues

- Minor skin rashes, pink eye

- Medication refills & follow-ups

- Mild GI upset

Go in-person for

- Chest pain, severe shortness of breath

- Serious injury, heavy bleeding

- Neurologic symptoms (stroke signs)

- Anything emergent → ER

Want $0-copay telehealth on your plan?

We’ll verify your network, show real costs, and compare Marketplace vs. Private PPO options for your ZIP.

Quick FAQs

Is telemedicine covered?

Many plans cover telehealth at 100% for non-emergency visits. We’ll confirm your exact copay and vendors.

Can telehealth prescribe meds?

Yes—for appropriate conditions. Controlled substances typically require in-person evaluation per state rules.

Does telehealth replace my PCP?

No. It complements primary care and urgent care for quick, non-emergency needs.

Robert Adams

RKA Insurance Advisors • Private & Marketplace Health Coverage • 561-806-9913 • robert@rkainsuranceadvisors.com