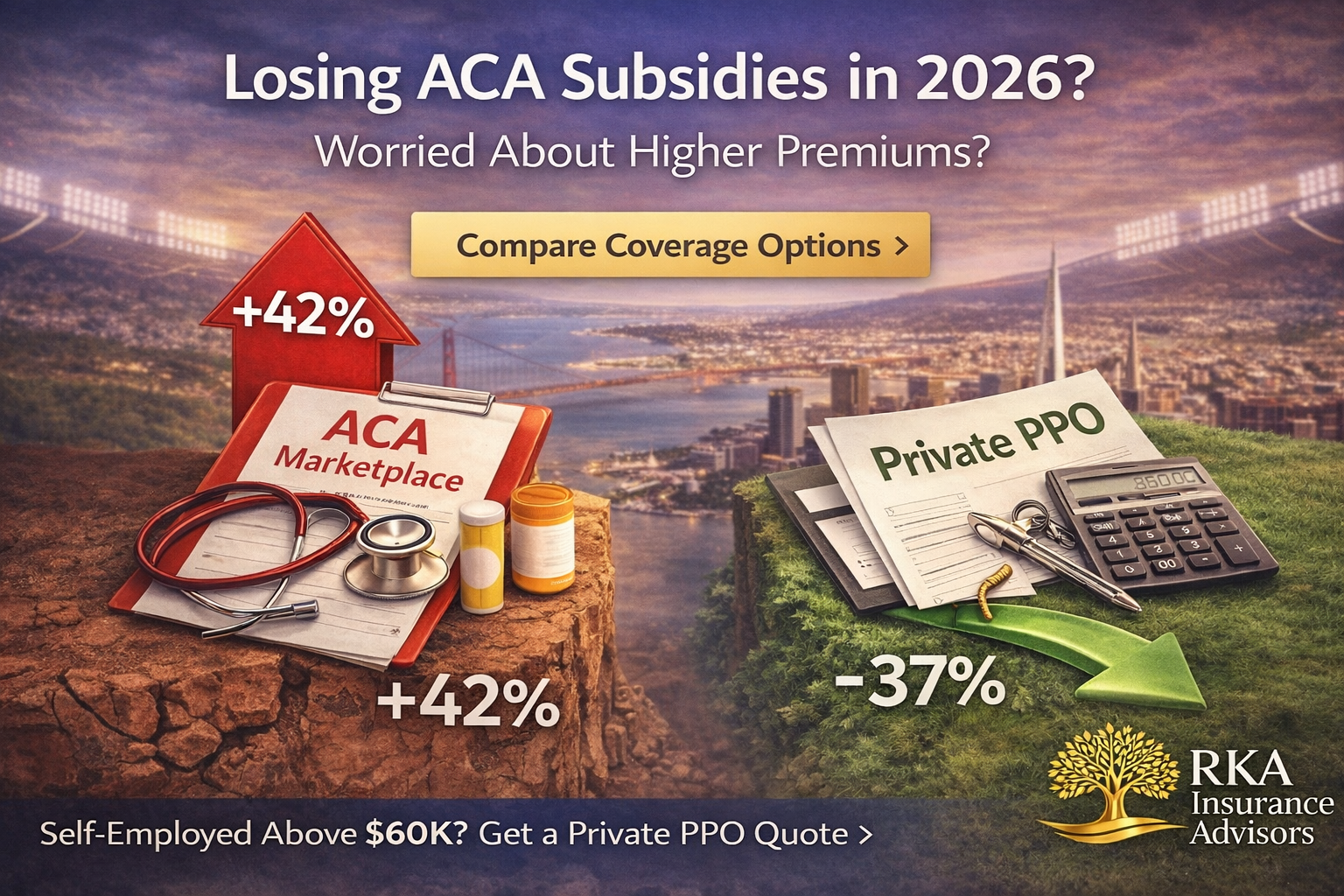

ACA Subsidy Cliff 2026: What Self-Employed Earners Above $60K Need to Know

Enhanced ACA subsidies expired December 31, 2025. If you earn above $60,240, you now pay the full unsubsidized Marketplace premium. Here's what changed — and what self-employed professionals in good health can do about it.

Private PPO * ACA 2026 * Self-Employed

ACA Subsidy Cliff 2026: What Self-Employed Earners Above $60K Need to Know

What changed in 2026

Before (2021-2025)

- Enhanced credits capped premiums at 8.5% of income

- Subsidies available at any income level

- Higher earners still got meaningful help

Now (2026)

- Subsidies cut off at $60,240 (individual)

- Above that - 100% full unsubsidized rate

- Full-price Silver plans average $600-$900/mo*

- Deductibles typically $4,000-$8,000

Marketplace vs Private PPO

- Guaranteed issue - no health screening

- Subsidies if income under $60,240

- Often HMO/EPO - referrals common

- Open enrollment window only

- Income reconciliation at tax time

- Full price if above subsidy threshold

- Health underwriting required

- Premiums based on health - not income

- Nationwide PPO access - no referrals

- Available any month - no enrollment window

- No subsidy reconciliation at tax time

- Can cost significantly less for healthy applicants*

Who Private PPO works best for

Income above $60K

- No subsidies available anyway

- Private PPO often cheaper

Variable income

- No mid-year reconciliation risk

- Fixed premium regardless of earnings

Missed open enrollment

- No qualifying event needed

- Coverage can start within days

How RKA helps

What we do

- Confirm your exact subsidy eligibility

- Verify your doctors in both ACA and PPO networks

- Project total annual cost - premium + deductible

- Pre-screen PPO eligibility before you apply

What you get

- Side-by-side ACA vs PPO comparison

- No surprises at application or tax time

- Coverage that fits your income and health

- A licensed advisor - not a call center

We verify your doctors, check your prescriptions, and compare ACA vs private PPO with real numbers. No pressure, no obligation.

Frequently Asked Questions

What is the ACA subsidy cliff in 2026?

The income point where premium tax credits phase out entirely - $60,240 for individuals in 2026. Earn $1 above that and you pay the full unsubsidized rate.

Are private PPO plans available if I missed open enrollment?

Yes. Private medically underwritten PPO plans are available year-round. No qualifying life event required.

How much could I save with a private PPO?

It depends on your age, state, and health history. For healthy applicants above the subsidy threshold, savings can be significant. We run the exact comparison for your situation at no cost.

What does medically underwritten mean?

The insurer reviews your health history before approving coverage. We pre-screen your eligibility so you know where you stand before submitting a full application.

Robert Adams * President & Licensed Agent * NPN 19540130 * Licensed in 30 states. For educational purposes only. *Premium estimates based on publicly available 2026 rate data and vary significantly by age, state, and plan. Speak to a licensed advisor for exact figures.

Amazon Layoffs & Your Health Coverage: Why COBRA Is Too Expensive and What to Do Instead

After Amazon layoffs, many workers face COBRA sticker shock. Learn how to cut costs and keep coverage using ACA or private PPO alternatives.

Nov 21 • Written by Robert Adams

Amazon Layoffs & Your Health Coverage: Why COBRA Is Too Expensive and What to Do Instead

Fast take: After Amazon layoffs, COBRA makes you pay the full employer plan cost—often hundreds more per month. With subsidy uncertainty and rising rates, many households can cut costs by switching to ACA or private PPO options during their Special Enrollment window.

Need help choosing the best plan after a layoff?

We’ll verify your doctors and prescriptions, compare ACA vs. private PPO options, and show clear costs—no pressure, just answers.

What’s driving the cost spike?

- COBRA = full freight. You carry the employer share + your share + up to 2% in admin fees.

- Subsidy uncertainty. Federal budget fights threaten enhanced credits, raising net premiums for many.

- Network fit. Employer HMOs can be narrow; qualified PPOs may provide better access for travel/specialists.

Moves to make now

- Protect your window. Job loss triggers a Special Enrollment Period (typically 60 days). Don’t let it lapse.

- Bring the details. Providers (names/locations), prescriptions (dosage), and your expected 2026 MAGI.

- Compare side-by-side. We’ll model COBRA vs. ACA vs. private PPO with total annual cost (premium + likely usage).

- Choose for access & price. Keep doctors in-network and avoid surprise Rx tiers.

How RKA helps laid-off Amazon employees

- Plan comparisons: ACA vs. PPO analysis with transparent cost projections.

- Network checks: We verify your doctors and hospitals are covered.

- Quick enrollment: Avoid gaps and set your 2026 pricing now.

Secure your 2026 coverage today

Quick FAQs

Is COBRA ever the right move?

Yes—short gaps, complex care mid-treatment, or high incomes (reduced subsidies) can justify COBRA. We’ll model it honestly.

Can private PPOs beat COBRA?

Often. If you qualify underwriting, PPOs can provide nationwide access at a lower net cost.

What if I miss my SEP?

We’ll use Open Enrollment timing and check paths that may reopen eligibility.

Robert Adams

RKA Insurance Advisors • Private & ACA Health Coverage

561-806-9913 •

info@RKAinsuranceadvisors.com •

Book an Appointment

For education only; eligibility and benefits vary by carrier and state. Always review official plan documents.

2026 Premium Explosion: What to Expect and How to Protect Your Wallet | RKA

ACA premiums are projected to spike in 2026 — the steepest rise in years. Here’s what’s driving the increase and how to protect your wallet before Open Enrollment.

2026 Premium Explosion: What to Expect & How to Protect Your Wallet

Why premiums are spiking

- Medical inflation: Higher hospital and provider costs are baked into 2026 premiums.

- Prescription drugs: Specialty medications like GLP-1s are a major cost driver.

- Policy changes: Enhanced subsidies may expire, raising net costs for millions.

How much higher?

Experts estimate average increases of 10–18% nationwide — with some states seeing much more. That means a plan costing $1,200/month today could jump by $150–200. For unsubsidized families, the hit could be thousands annually.

Smart moves before 2026

- Compare Marketplace vs PPO: Don’t assume Healthcare.gov is always cheaper. Private PPOs may win if you don’t qualify for subsidies.

- Check your eligibility: Income-based savings may still apply — know your bracket.

- Time your enrollment: Lock in your plan during Open Enrollment this fall before further adjustments hit.

Get Expert Guidance Today

We’ll verify your doctors and prescriptions, compare Marketplace vs. Private PPO, and show clear costs — no pressure, just answers.

Quick FAQs

Why are ACA premiums going up in 2026?

Medical inflation, rising drug prices, and subsidy uncertainty are driving rates higher than in prior years.

How much more will I pay?

Average increases are expected to be 10–18%, with unsubsidized households seeing the steepest jumps.

Can private PPOs be cheaper than Marketplace?

Yes. If you don’t qualify for subsidies, PPO options may offer better value, especially with nationwide networks.

When should I enroll?

During Open Enrollment 2026. Lock in your coverage early before mid-season adjustments hit.

How do I protect my wallet?

Compare all your options now, confirm your doctors are covered, and work with a licensed advisor.

Bottom line

2026 premiums will be some of the highest on record. The best protection is preparation — comparing options, confirming your doctors, and working with a licensed advisor. Don’t wait until the last minute to make changes that could save you thousands.

Need help navigating 2026 premium increases? Our licensed advisors compare marketplace and private PPO health insurance options to find coverage that fits your budget. Get personalized quotes from our team.

Montana 2026 Health Insurance Premiums: What to Do Before Prices Jump | RKA

Montana health insurance premiums are projected to rise in 2026, with insurers citing higher medical costs and subsidy uncertainty. Families could see significant changes in out-of-pocket costs. Here’s what to know—and how private PPO options may help you save before rates jump.

Montana • Premium Watch

Montana 2026 Health Insurance Premiums: What to Do Before Prices Jump

Fast take: Montana insurers have filed for notable premium increases for 2026. Rising medical costs, specialty drugs, and subsidy uncertainty could push net prices higher. Here’s how to prepare and compare now.

What’s driving the increase?

- Medical inflation: Higher provider costs and hospital charges are impacting trend.

- Specialty drugs: Expensive medications like GLP-1 therapies are raising premiums.

- Policy shifts: Enhanced ACA subsidies may expire, impacting net household costs.

Moves to consider now

1) Review your plan type

If you travel across state lines, a nationwide PPO may provide broader access and lower surprise costs than an HMO.

2) Time your enrollment

Open Enrollment later this year sets your 2026 price. We’ll help compare ACA and private PPO options side by side.

3) Explore private PPO eligibility

Private, medically underwritten PPOs can offer lower premiums for healthy households. We pre-screen underwriting and confirm provider networks.

How RKA helps Montana families

- Plan comparisons: ACA vs. PPO side-by-side analysis.

- Network checks: Verify your doctors and hospitals are covered.

- Quick enrollment: Avoid coverage gaps and set 2026 pricing now.

Quick FAQs

Will 2026 premiums apply to my plan immediately?

Are PPOs available in Montana?

Can RKA confirm if my doctors are in-network?

For education only; eligibility and benefits vary by carrier and state. Always review official plan documents.

Extended Open Enrollment Information

Open Enrollment has been extended through January 15, 2026. Don't miss your last chance to enroll in Marketplace or Private PPO health insurance for 2026. Get free quotes from licensed advisors today.Extended Open Enrollment: Don't Miss the January 15th Deadline

Good news! You still have time to get health insurance for 2026. Open Enrollment has been extended through January 15, 2026, giving you 30 extra days to compare plans and enroll with confidence.

⚠️ Important: If you missed the December 15th deadline for January 1st coverage, you can still enroll by January 15th for coverage starting February 1, 2026.

Key Enrollment Dates

The federal Open Enrollment period for 2026 began November 1, 2025 and closes January 15, 2026. This extended timeline gives you more time to:

- Compare Marketplace and Private PPO plan options

- Verify your doctors and prescriptions are covered

- Calculate your subsidy eligibility

- Enroll with a licensed advisor at no cost to you

What's Available for 2026?

There are several health coverage options available during Open Enrollment:

- Marketplace Plans (Healthcare.gov): ACA-compliant plans with potential income-based subsidies

- Private PPO Plans: Off-exchange underwritten options with broader networks, available only through licensed agents

- Ancillary Coverage: Vision, dental, accident, critical illness, and short-term disability

Why Work With a Licensed Advisor?

Health coverage is too important to navigate alone. Working with a licensed health insurance advisor ensures you:

- See all available options — both on and off the marketplace

- Get accurate subsidy calculations based on your income

- Have your doctors and prescriptions verified before enrollment

- Receive year-round support for claims, renewals, and coverage changes

Best of all, there's no cost to you. Licensed agents are compensated by insurance carriers, not by clients.

Ready to Compare Your Options?

Don't wait until the last day — get your free quote today

What Happens After January 15th?

After Open Enrollment closes, you'll need a Qualifying Life Event to enroll in Marketplace plans. Common qualifying events include:

- Loss of employer-sponsored coverage

- Marriage or divorce

- Birth or adoption of a child

- Permanent move to a new state or county

- Loss of Medicaid or CHIP coverage

Important note: Private PPO plans may be available year-round depending on your health status and location. Contact us to explore your options even after the Open Enrollment deadline.

Need help before the deadline? Call us at 561-806-9913 or get your free quote online. We're licensed in 32 states and ready to help you find the right coverage.