Open Enrollment 2026: What You Need to Know

Oct 15 • Written By Robert Adams

Fast take: ACA health plan rates and benefits can change for 2026. Open Enrollment is your yearly window to switch plans, verify your doctors, and lock in coverage dates. Here’s the 2-minute rundown and how we’ll compare options for you.

Important dates

Open Enrollment Window

Nov 1, 2025 → Jan 15, 2026

Enroll by Dec 15

Coverage starts Jan 1, 2026

Enroll by Jan 15

Coverage starts Feb 1, 2026

Get Expert Guidance Today

We’ll verify your doctors and meds, compare Marketplace vs. Private PPO, and show clear costs—no pressure, just answers.

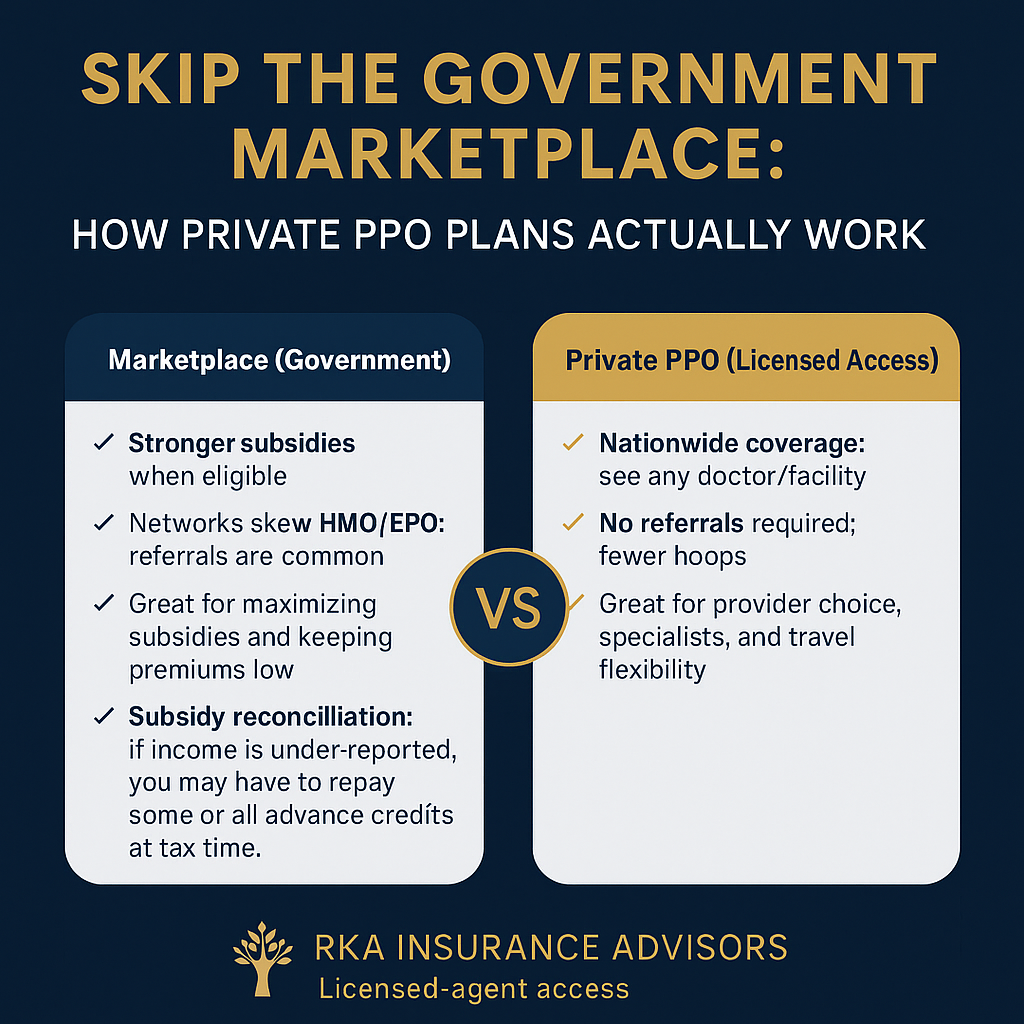

What’s changing for 2026?

- Medical inflation & utilization: Hospital and provider costs continue to ripple through next year’s premiums.

- Prescription drugs: High-cost specialty meds remain a driver; formularies and tiers can shift.

- Subsidy math: Income and household size determine savings. We’ll confirm your eligibility band before you choose.

- Networks: HMO vs PPO vs EPO—pick based on the doctors/hospitals you actually use, not just the premium.

How to choose the right plan (quick framework)

- Doctors & facilities first: We confirm in-network status and referral rules.

- Rx check: We price your actual meds across plans (tier, prior auth, step therapy, mail-order).

- True annual cost: Compare premium + expected usage (copays/coinsurance + deductible + max out-of-pocket).

- Access & travel: If you need multi-state flexibility or out-of-network options, consider PPO over HMO.

Quick FAQs

When should I enroll?

Enroll early. Dec 15 starts Jan 1 coverage; Jan 15 starts Feb 1 coverage.

Can private PPOs be cheaper than Marketplace?

Yes—especially for healthy households that don’t qualify for large subsidies. We’ll model both paths.

Can you confirm my doctors and hospitals?

Absolutely. We verify providers and prescriptions before we present options.

Bottom line

Open Enrollment 2026 is your chance to realign cost, access, and coverage. We’ll do the homework—net cost, doctors, medications, and network rules—so you can enroll with confidence.

Robert Adams • President & Licensed Agent • NPN 19540130

Licensed in AL, CO, DE, FL, GA, IA, IL, IN, KY, KS, LA, MD, MI, MO, MS, MT, NC, NE, NV, OH, OK, SC, SD, TN, TX, UT, VA, WI, WV, WY

For education only; eligibility and benefits vary by carrier and state. Always review official plan documents.